2024: Year of Indian Contrast

How India's Equity Cult is Making its Financial Markets Vibrant!

As we approach the end of 2024, the strongest evidence of the decoupling of Indian markets has emerged this year from the primary markets, which we are focusing on in today’s blog. We hope you enjoy reading it - let’s get started!

Has India Decoupled?

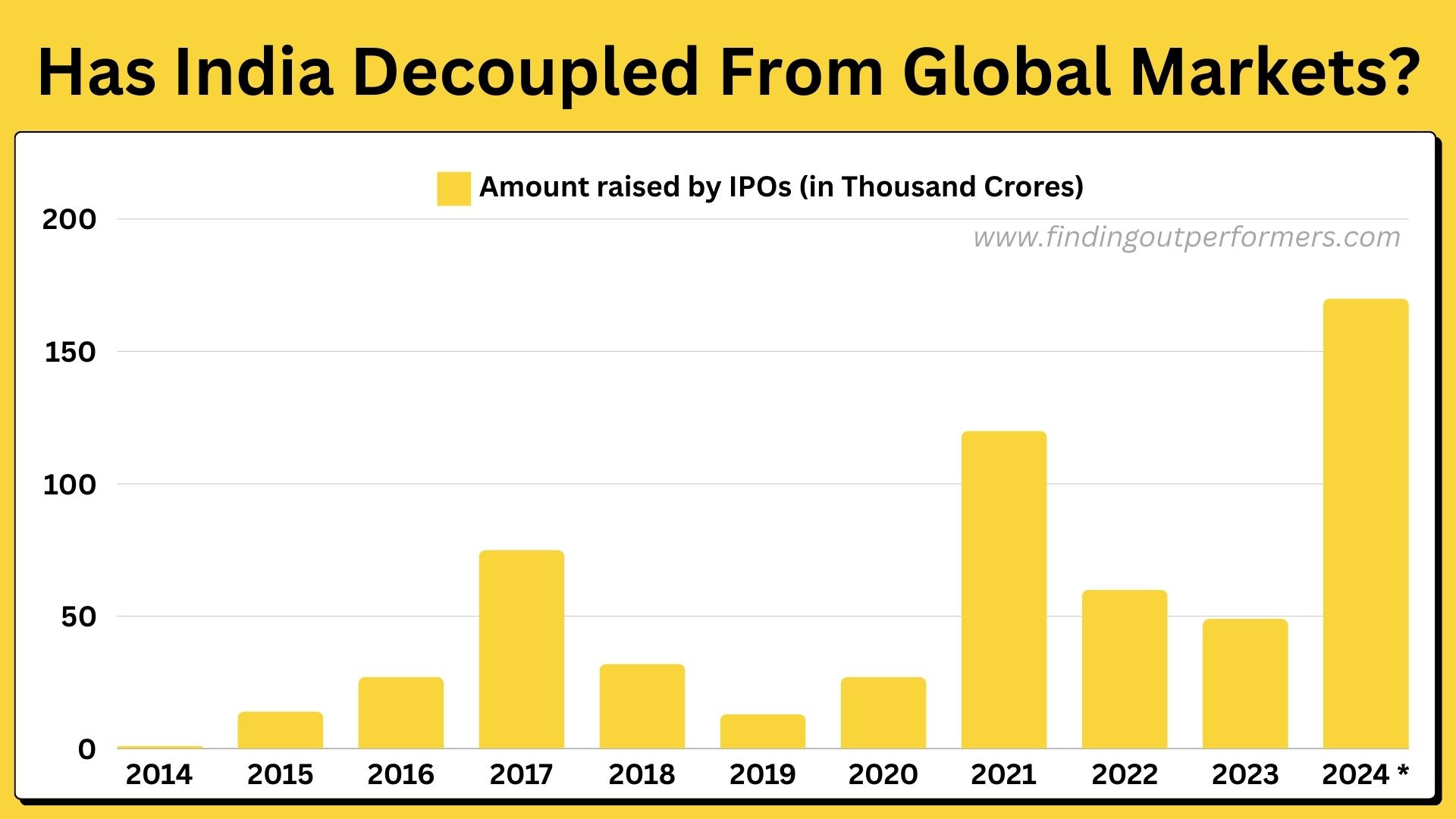

The amount raised in India by IPOs in 2024 is set to touch $20 Bn, marking a fresh peak and significantly surpassing the previous high of 2021, which was driven by excess global liquidity. What’s surprising is the stark contrast with the developed markets, which remain significantly below their peak.

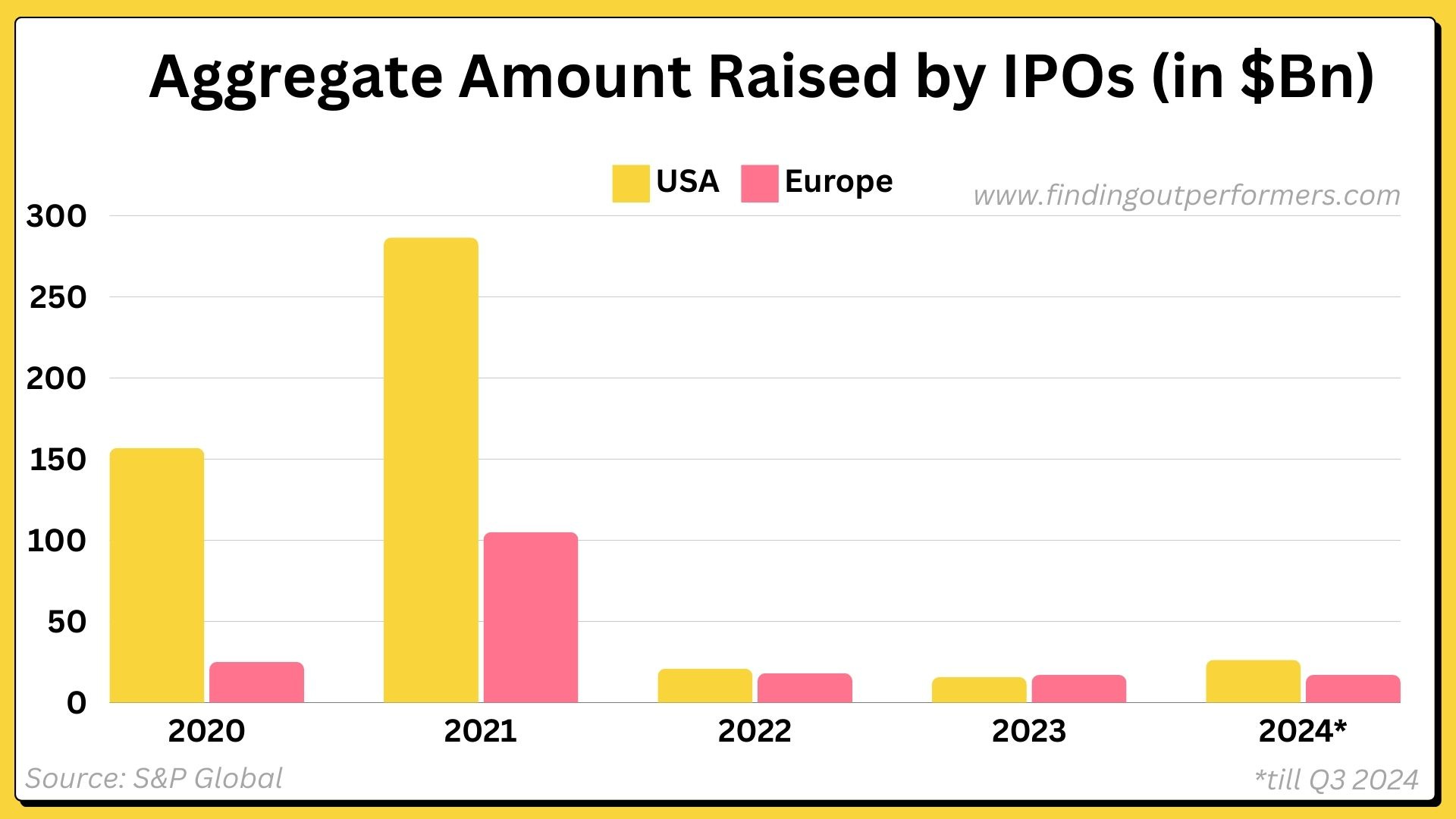

Let’s take a closer look at the U.S. & European primary markets since 2020:

The boom that began in the second half of 2020 and extended through 2021, fueled by excessive liquidity from central banks worldwide, propelled the U.S. IPO market to record levels. Notable offerings included Airbnb, Snowflake, and Rivian, while in Europe, companies like Deliveroo and Wise raised billions despite mixed post-IPO performances.

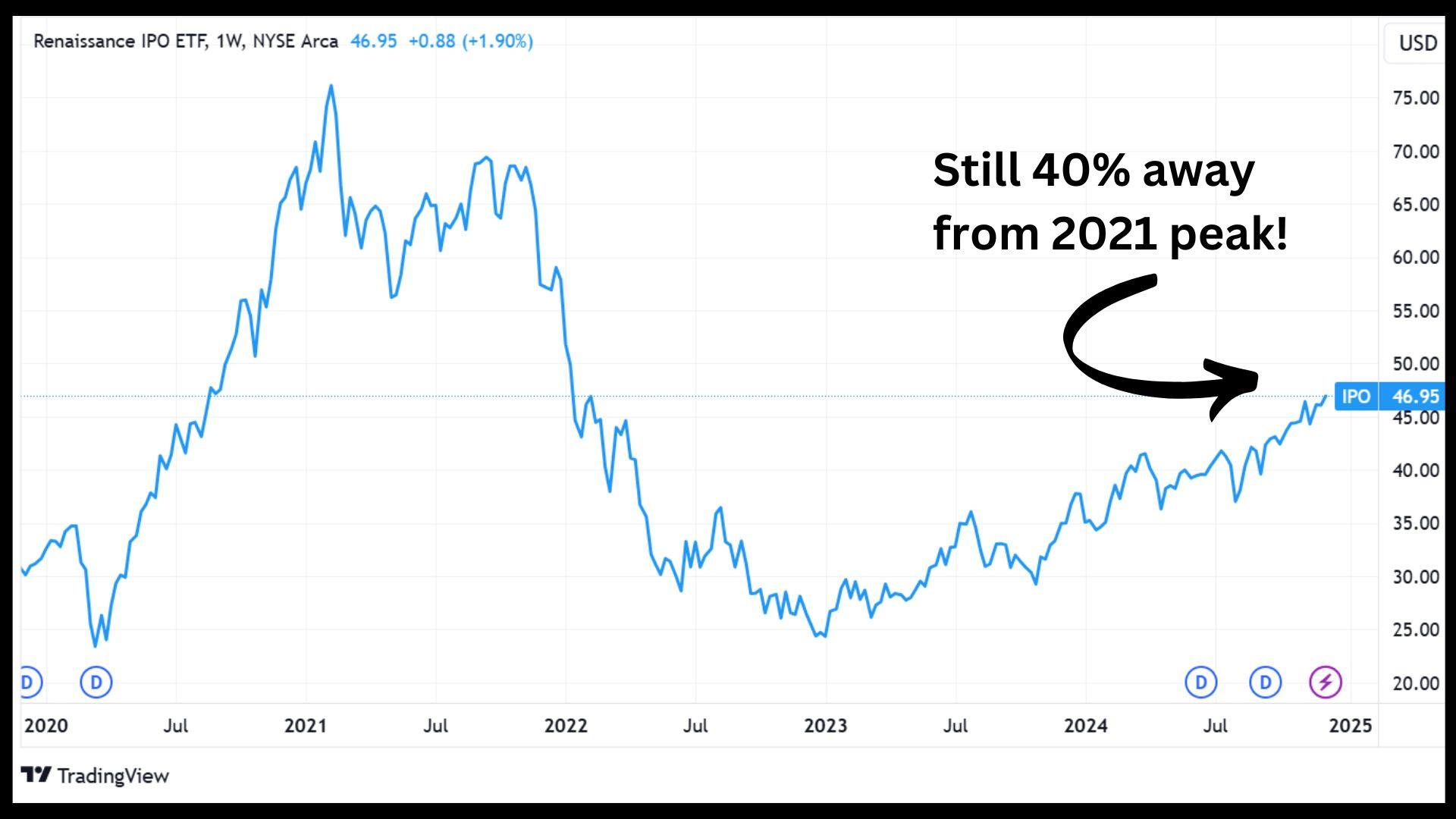

However, as the liquidity tap dried up, both secondary market valuations and primary listings suffered. For instance, Instacart (Maplebear Inc.) went public in September 2023 at a valuation of $9.9 Bn, a sharp decline from its peak private valuation of $39 Bn. There is also an traded ETF in U.S. which tracks performance of newly listed companies which shows how companies performed post listing.

Renaissance IPO ETF: This ETF offers access to newly public U.S. companies, aiming to capture returns from innovative businesses post-IPO. Companies are included shortly after their IPO and removed after three years of trading. It rebalances quarterly and focuses on the largest and most liquid IPOs.

While the S&P 500 recorded more than 57 record closing high for 2024, the IPO ETF remains 40% below its peak from 2021.

Another notable point is that IPO activity in the U.S. tends to rise significantly in post-election years, averaging a 39% increase (219 IPOs) compared to election years (149 IPOs) and a 24% increase compared to other non-election years (176 IPOs). With pro-capitalist Republicans winning the 2024 elections, a surge in public listings is anticipated in 2025.

2024 - The Indian Contrast (Part 1)

While the U.S. and European markets faced challenges, the trend in India has been completely opposite. Indian primary markets are setting a new record in 2024 by raising approximately $20 billion - 40% higher than the previous peak achieved in 2021, which was driven by global liquidity.

In 2024, India witnessed landmark IPOs, including Hyundai’s Korean parent listing its Indian arm on domestic exchanges, raising over $3 Bn entirely through an offer for sale. Swiggy’s IPO, the largest tech IPO in India raising $1.34 Bn, followed closely by NTPC Green’s $1.2 Bn offering, the biggest in India’s renewable energy sector by the government-owned NTPC’s arm.

Looking ahead, 2025 holds a promising IPO pipeline with notable names like India’s largest private bank - HDFC Bank’s subsidiary HDB Financial, LG’s Indian arm, and several others set to hit the market.

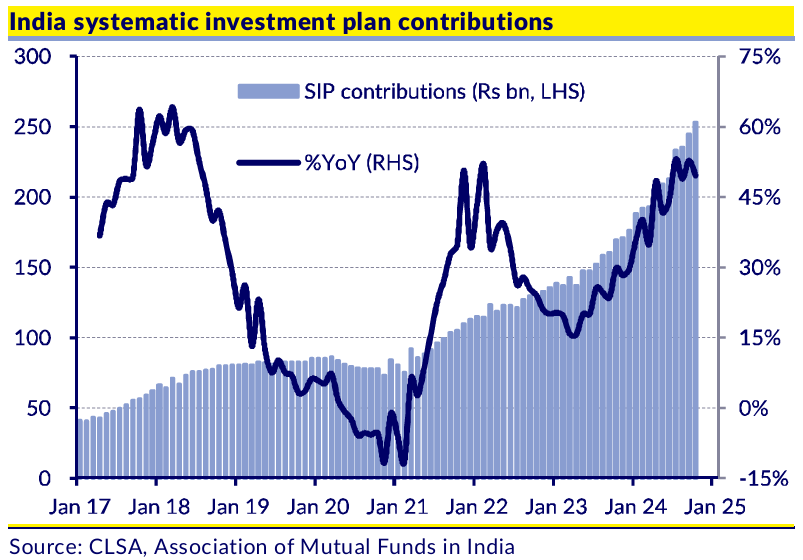

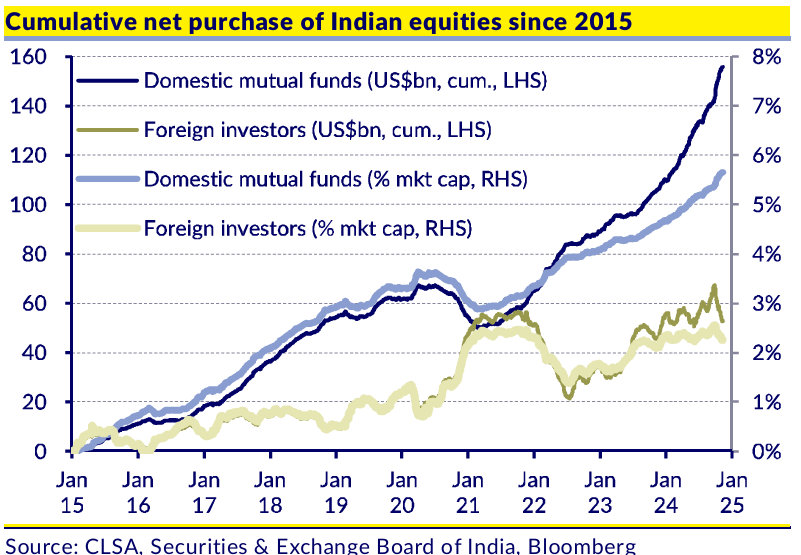

A key driver of India’s contrasting primary market performance compared to developed markets is the strengthening equity culture. The public’s inclination towards equity as an asset class has grown tremendously, with a shifting attitude that now views the stock market not as a mere “satta bazaar” (betting market) but as a reliable long-term wealth creation tool.

The robust momentum of monthly SIPs (Systematic Investment Plans) has significantly boosted domestic ownership of Indian equities.

According to SEBI estimates, the Indian Mutual Fund industry has cumulatively purchased equity shares worth $160 Bn over the last decade - over 5% of India’s total market capitalization. Notably, Indian equities are now 83% domestically owned, with promoters remaining the largest stakeholders. This is the highest domestic ownership proportion among emerging markets.

Listing on New York vs. local stock exchange

Ringing the NYSE bell in the United States is a dream for many tech entrepreneurs. For countless startup founders worldwide, Silicon Valley serves as the ultimate source of inspiration. With listed tech giants valued at trillions of dollars and unlisted startups raising millions and billions from deep pools of PE/VC funds eager to support innovative ideas, the U.S. often seems like a paradise for aspiring global entrepreneurs.

Interestingly, the largest IPO in U.S. history by size wasn’t from an American company but the Chinese giant Alibaba. In 2014, Alibaba chose to list on the New York Stock Exchange instead of Hong Kong or China, debuting with a staggering valuation of over $160 Bn and raising $25 Bn (including options)—a record that still stands today!

Although Alibaba had a secondary listing in its home country in November 2019, its decision to initially list abroad highlights a missed opportunity for China’s domestic financial system. When a prominent leader in e-commerce and payments opts for a foreign listing, it should be seen as a setback for the local ecosystem and here is why domestic listings are vital:

Domestic listings enhance the depth and liquidity of local capital markets, attracting more investors and fostering a robust financial ecosystem. A vibrant local stock market can spark a virtuous cycle of domestic wealth creation and reinvestment, making it easier to fund innovative and risk-taking ideas.

Domestic listings are often more straightforward compared to foreign ones. Successful large-scale listings on local exchanges at favorable valuations serve as a positive signal to Private Equity and Venture Capital, encouraging them to invest for long term with greater confidence due to higher chances of profitable exits.

Keeping future tech giants listed locally ensures that the country retains a degree of control & oversight over its critical industries. This is especially important for safeguarding national interests, including data protection and strategic autonomy.

Prominent domestic IPOs often become a source of national pride, helping to build a positive narrative about the country’s economic strength. It’s important to recognize that not every company can list on U.S. exchanges. When a major local company chooses to list abroad, it can inadvertently diminish the credibility and attractiveness of the domestic exchange. This sets a precedent, encouraging other companies to look outside for their listings, potentially weakening the local financial ecosystem.

While China’s e-commerce giants like Alibaba and JD.com chose U.S. listings a decade ago, India has the privilege of seeing its E-commerce giants (read Quick commerce) are now listed domestically. Companies like Zomato and Swiggy have already made their mark on Indian exchanges, and Zepto is hopefully next in line! This trend underscores India’s ability to retain its homegrown champions while building its financial markets.

2024 - The Indian Contrast (Part 2)

Following the IPO listing contrast highlighted in Part 1, the impact is now visible in bringing back startups that had previously domiciled outside India for tax-saving reasons or with plans for future foreign listings. As India strengthens its domestic financial ecosystem and offers favorable conditions for local listings, these startups are now more inclined to return and list on Indian exchanges, contributing to the growth and credibility of the local market.

𝐑𝐞𝐯𝐞𝐫𝐬𝐞-𝐅𝐥𝐢𝐩𝐩𝐢𝐧𝐠: An increasing number of major Indian unicorns who were registered in foreign countries including PhonePe, Groww, Pepperfry, Razorpay, Pine Labs & Meesho are now coming back/have already domiciled themselves in India in 2024. While amongst the key reason for this shift is the ability of Indian markets to list tech companies on domestic indices - other contributing factors include clarification by government on tax laws which has made the absence of tax advantage evident in certain scenarios. The fact that multiple start-ups have become household names, yet the Indian public wouldn’t be able to participate in their IPOs due to these companies being overseas entities, is also a major reason for the shift back.

Does it make a difference?

While foreign listings may bring in dollars from IPO proceeds strengthening local currency, large listings in domestic markets can lead to liquidity being drained from the system, which can also affect domestic banks. So, why not prefer foreign listings?

That’s a short-sighted perspective. For the sake of short-term gains, we shouldn’t allow our financial markets to stagnate, as we've seen in other markets like the UK and Singapore. We need a vibrant, expanding ecosystem with diverse investors that can support the innovation shaping India’s future. A future led by tech companies should not feel the need to list abroad. This is precisely what makes the U.S. the financial hub of the world where tech from across the world goes to list themselves.

Take the case of a 2023 listing of Arm Holdings, Softbank owned semiconductor company:

Arm Holdings was previously listed on the London Stock Exchange (LSE) from 1998 until 2016, when it was taken private by SoftBank Group. In 2023, Arm Holdings went public on the NASDAQ in the U.S. at valuation of $54 Bn and was seen as the biggest IPO event of the year.

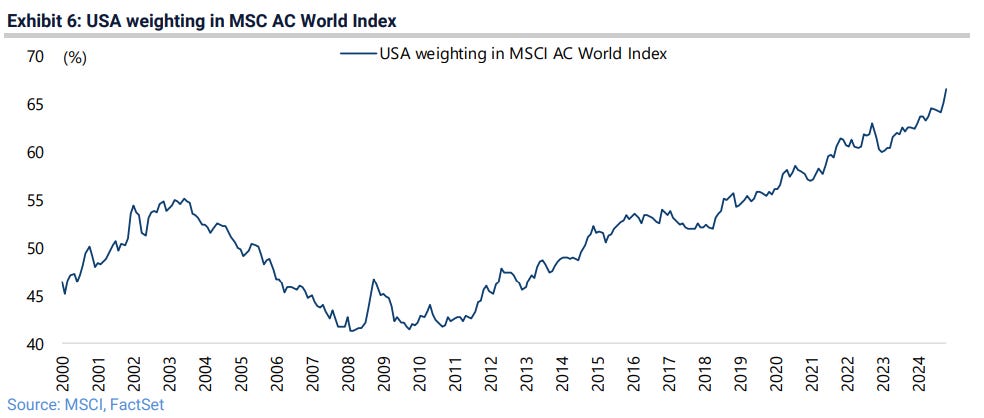

Incidentally, the weight of U.S. stocks in the MSCI All Country World Investable Market Index (ACWI IMI) has now reached a record high of 67%:

In fact, India reached Rank 6 in terms of its weight in this index, crossing China and Taiwan as per mid September 2024 list of Top 10 Weighted countries - this keeps on fluctuating though.

“India will continue to gain share due to market outperformance, new issuance and liquidity improvements.”

- Jonathan Garner, Chief Equity Strategist for Asia & EM, Morgan Stanley

Fresh issuances, such as IPOs, increase the market weight, which in turn attracts greater foreign flows into the country.

Biggest Risk?

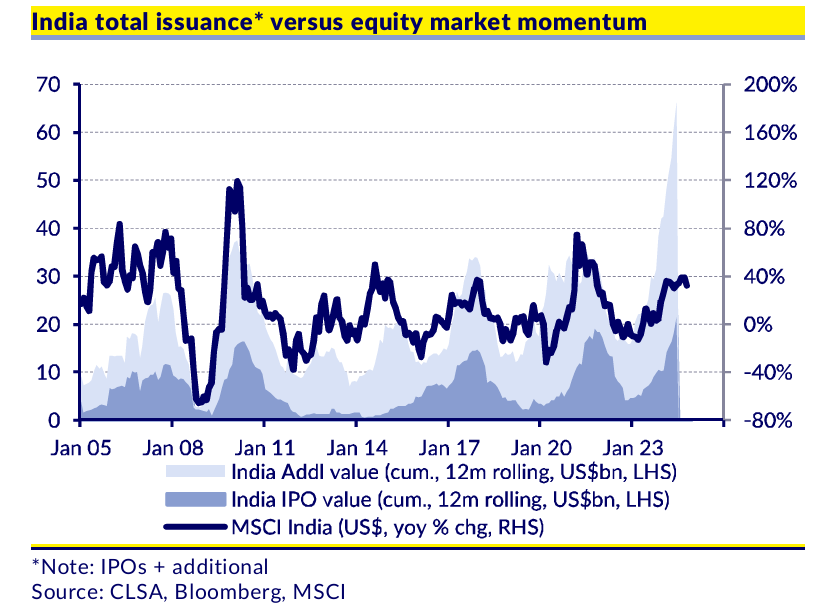

As CLSA aptly puts it, “Suffering from Success” - the risk of suffocation from primary flows is real. While the amount raised from IPOs has already reached a new high in 2024, secondary market transactions are also on the rise, surpassing $70 Bn as of December 2024 - double its previous peaks!

With a substantial pipeline of IPOs set to hit the market in 2025, the question remains: Will the momentum of domestic flows continue to rise to sustain this growth, or will the cycle slow down significantly in 2025 alongside impacting valuations in secondary market? We shall continue to track emerging developments closely.

That’s it for today. Connect with me (Aditya here) and my co-author Yash here.

Finding Outperformers is a free-to-access website, and each blog takes a month of effort to finalize. If you've read this far and you find our research useful, consider supporting our efforts by contributing here:

Read our latest publications:

| A guest post by

|