Rebirth of PSUs

Disinvestment to Wealth Management | Power Consumption to Coal India

Hey there!

Government-owned listed company stocks, known as Public Sector Units (PSUs), have become favorites of Indian stock market bulls since the COVID-19 pandemic in 2020. After years of underperformance, a trend reversal seems evident. Just recently again, they grabbed headlines as their share in India's total listed market capitalization crossed 10%, reaching a 7-year high!

Before discussing the returns generated by PSU stocks, it's crucial to acknowledge one of the main factors behind their increase in % share of total equity market cap: the listing of various government entities such as LIC, IREDA, and others. The listing of India's largest insurer, LIC, with a market capitalization of approximately 6 lakh crores, has notably contributed to the increased PSU share in India's total market capitalization, which stands well over 300 lakh crores today.

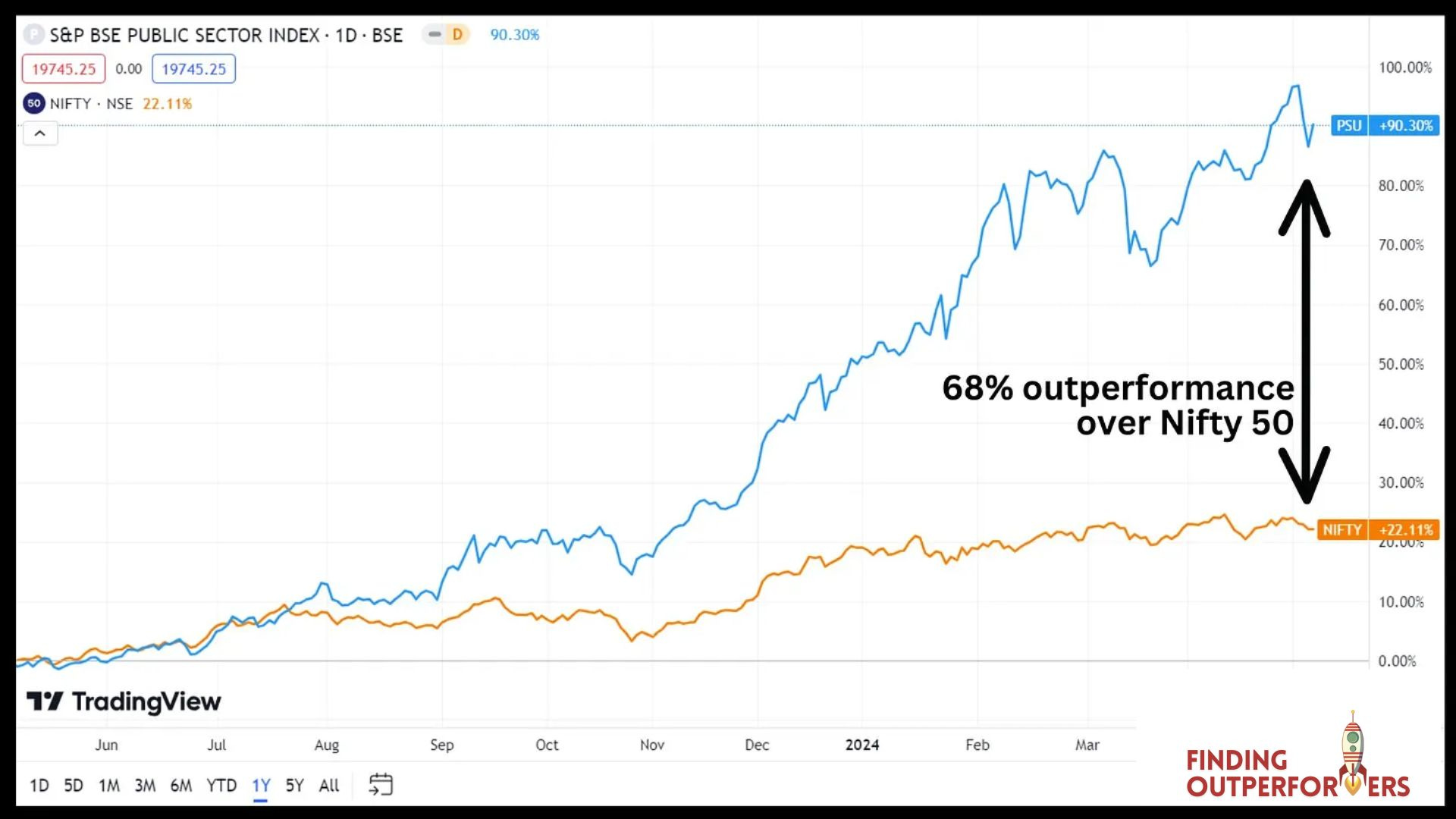

On the returns front, the BSE Public Sector Index, comprised entirely of PSUs, has outperformed the headline Nifty 50 index by approximately 70% in just one year. This outperformance surpasses that of small-caps and mid-caps as well.

Fortuitously, approximately a year ago, we made the decision to invest in our first PSU stock (and also wrote about it), which has more than doubled in value since then and provided us with a 10% dividend yield on our initial investment within the same timeframe (For more details, see "Why we recently invested in Coal India?"). We will further elaborate on our positive outlook for Coal India in the conclusion of today’s blog

Note: If our emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out on future blogs. Don’t forget to subscribe and join 1K+ readers!

Disinvestment: A complete disappointment?

During the presentation of our FY22 budget by Nirmala Sitharaman in February-March 2021, the government signaled a shift in strategy towards expediting the sale of non-strategic PSU entities, commonly referred to as privatization/disinvestment. While this wasn't a novel initiative or a drastic change in governmental policy, it became apparent that they were determined to push through the privatization of non-strategic entities, including notable ones like BPCL, at any cost. Prime Minister Modi echoed this sentiment on disinvestment post the FY 2022 budget, asserting, "Government has no business to be in business…...it is not necessary and feasible in today’s era that the government should run the enterprises and continue to own it." The market reacted positively to these announcements, recognizing the potential value addition in terms of enhanced efficiencies and governance that private management often brings.

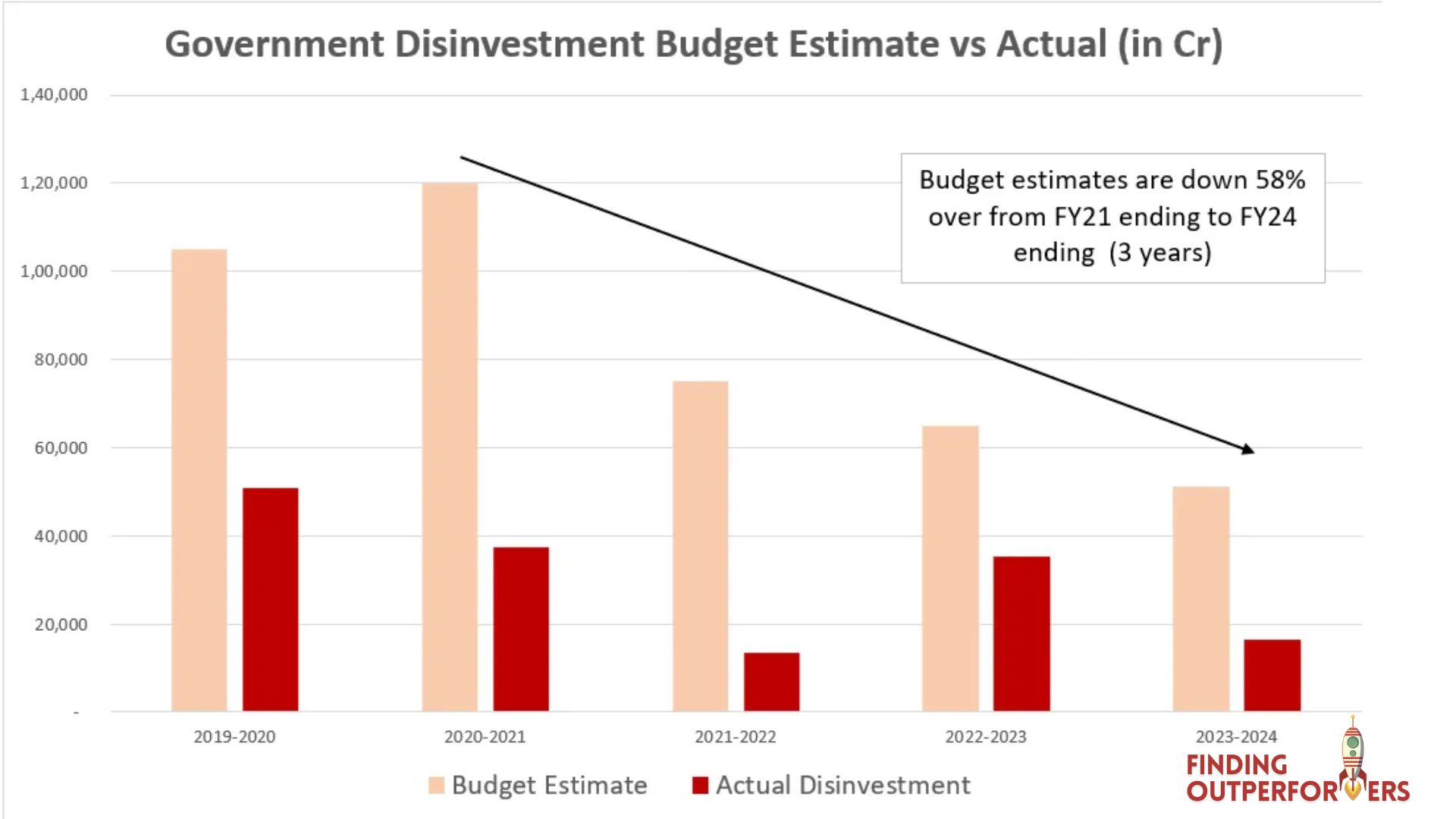

However, the reality of disinvestment over the past three years has been profoundly disappointing. We have consistently fallen short of our budgeted estimates in each of the last five years. Consequently, the government has significantly revised down its disinvestment targets by over 58% from FY21 to FY24

Sell-off to Wealth Management?

After a string of failures to meet its targets, the government not only scaled down those targets but also underwent a notable shift in approach from mere "sell-off" to a strategy centered around wealth management. The focus has now shifted towards optimizing the long-term value of public assets rather than simply divesting them. According to a government official (source: HT), there is a concerted effort to ensure that public assets are managed in a manner that maximizes their value over time.

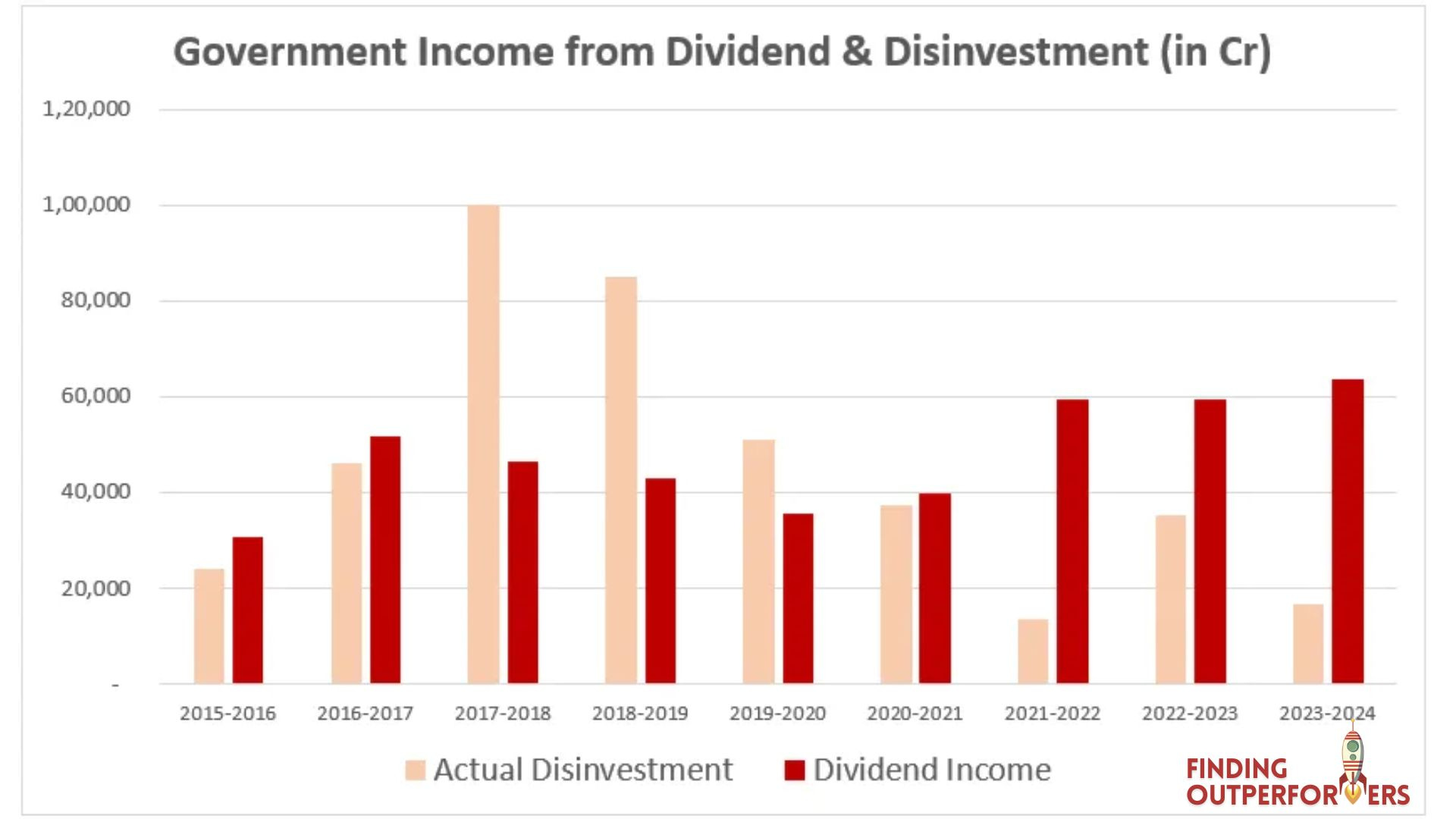

“We are making sure that valuations of each PSU entity are kept up, they are improved upon and markets should look them favorable” - Nirmala Sitharaman, Finance Minister of IndiaIn this interview, Nirmala Sitharaman also discusses the government's proactive efforts to enhance the performance of each PSU. She highlights a significant increase in dividends from PSUs over recent years. Despite a decrease in the government's percentage ownership in several key dividend-paying large PSUs before the COVID-19 pandemic, the government continues to accumulate substantial dividend sums. Consequently, in absolute terms, these dividends compensate for the shortfall resulting from the unmet disinvestment targets. Our team has prepared a chart based on data sourced from the Department of Investment and Public Asset Management (DIPAM), which operates under the Ministry of Finance - from their Capital-Restructuring archive and Past-Disinvestment archives:

So even after 3 years when our PM Modi and team expressed their thoughts on disinvestment after the FY 2022 budget was laid out, the government's disinvestment is down by 55% since then. One might tend to believe that PM Modi failed, but lets focus on these 2 key pointers as well:

1. A big chunk of the reduction in disinvestment has been compensated by the record dividend income from those very PSUs, which is now being received by the government. Hence, on overall/absolute basis, the government's receipts from PSUs in the form of 'Dividends + Disinvestments' have increased over the last four years, despite the government owning a lesser portion of its PSUs.

2. Upon delving deeper into PM Modi's messaging on disinvestment, one would realize that the government's primary objective was to alleviate the burden of loss-making public sector enterprises by divesting or turning them around, thereby curbing the wastage of taxpayer money on refinancing. This objective has been successfully achieved. For example :

>> Burden of funding Air India for its losses every year is now gone post-privatization

>> PSU Banks no longer require recapitalization - Capable of raising funds from open markets

>> Entities like BSNL are aiming to turn net profitable by FY2027

So, despite the inability to meet its disinvestment targets, the government hasn't failed entirely. Instead, it has managed to notably increase the value of its assets, thanks to some improvement on the governance front and higher-than-anticipated dividends.

Moving forward, let's shift our focus to power consumption potential in India and why we still have a positive outlook on Coal India within the PSU sector, despite the considerable rally we've witnessed. Let's dive in!!

Are we in a power super-cycle?

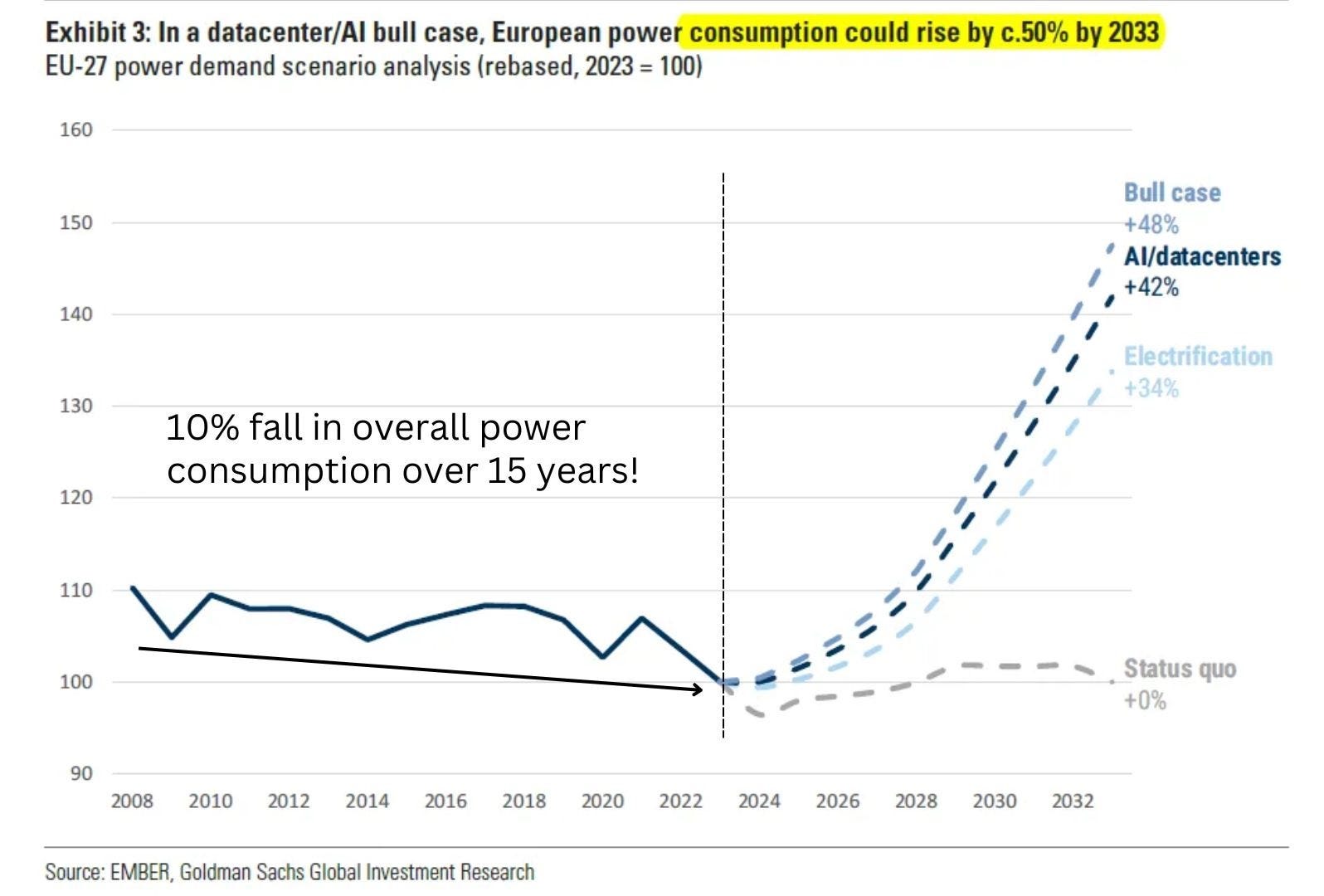

Over the past fifteen years, Europe’s power demand has cumulatively declined by nearly 10%. It has been severely hit by exogenous shocks (the Global Financial Crisis, Covid Crisis, and Energy Crisis), a slower-than-expected pick up in the electrification process, and by ongoing de-industrialization of the European economy, since the 2008 power consumption peak. But Goldman Sachs believes it’s soon going to reverse due to the impact of AI-Datacenters and Electrification.

The reason I brought this interesting chart up is due to the changing power consumption dynamics across the world. India’s growing power consumption has structural tailwinds to support it, but if the sunrise of new technology like Artificial intelligence and GPTs of the world implies a significant rise in power consumption in future, it would imply that the runway is huge for total power consumption growth for countries like India where per-capita consumption is amongst the lowest in the world! Electricity/power consumption in India has grown at a rate of 5-6% CAGR over the last decade which is a tad lower than the rate at which GDP has grown, but the impact on electricity consumption by AI and computation can cause a significant change in this growth rate for years to come. I hope we get to see Goldman Sach’s India-dedicated report soon.

Coal is still the Gold!

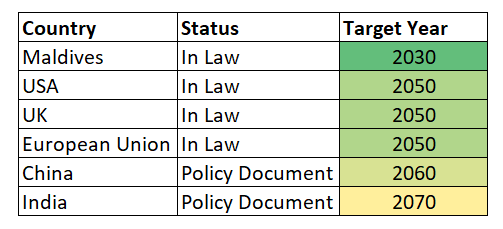

India currently relies on thermal energy (coal) to meet approximately 70% of its electricity requirements. While many major countries are aiming to achieve net-zero emissions by 2050, India has set a target to achieve this milestone by 2070. Remarkably, according to ECIU’s Net Zero tracker, no other country has declared a target year beyond 2070. This places India among the last countries to reach net-zero emissions, assuming all proposed targets are met:

While many countries worldwide are phasing out coal by shutting down their thermal plants, the situation in India is different. Despite the government's emphasis on green energy, the demand for power continues to grow rapidly. Consequently, PSUs like NTPC, the largest government entity in the power sector, are moving forward with plans to establish another thermal power plant in Uttar Pradesh, India. This initiative is aimed at meeting the escalating power demands in the medium term.

Coal India finally!

Here we come to Coal India - Our first non-banking PSU stock that was added to the Finding Outperformers portfolio in May 2023. Our view was clear - Coal India for us is one of the best dividend plays that can pay high dividends for years to come. If we have a look at the absolute value of dividends paid by Coal India in the last 10 years, one would realize that we are yet to see a new peak

With the government's renewed emphasis on PSU dividends, the potential for a power consumption super cycle, and India's ongoing reliance on coal, Coal India's current valuation of 9 times the forward Price to Earning ratio remains appealing to us. We anticipate the company could surpass market consensus in dividend payments in the upcoming years.

Biggest Risk to Coal India and PSU rally continues to be political uncertainty around the existing government of PM Modi coming back to power. We shall get to know about it in the coming weeks.

That’s it for today! Today’s blog was co-authored with Sanjana Chauhan

You can find me (Aditya) on LinkedIn here.

Wondering how you can support us?

If you find our content valuable & are willing to support, show some love here⬇️

Disclaimers-

We are not SEBI registered advisors; personal investment/interest in the shares exists for the company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome.

| A guest post by

|

The whole world seems to be power-hungry at this moment. Imo, the trend will continue. Even if we keep our energy consumption unchanged, the mode of consumption is tilting to electricity. If we need 50% electrification by 2050 we need 2.5X more power and this is without taking into account power guzzlers like data centers and desalination plants