Can Indian Rupee reach ₹80/$ level?

Part 1: Fast growing services trade surplus builds case for stronger currency

As we approach the close of the financial year 2024-25 this month, the Nifty 50 has delivered its highest weekly return of 6%, marking its best performance since February 2021. While the extreme pessimism in the markets over the last five months may explain the sharp rebound, what could have caused the shift in sentiment leading to this recovery is our focus today.

On March 17, 2025, India's trade data for goods and services was released, revealing a surprising drop in the trade deficit to $14 Bn, significantly lower than the expected $21 Bn. What followed after that was also Indian Rupee strengthen from sub - ₹ 87 levels to below ₹ 86/$ towards weekly closing, along with a sharp rebound seen in the stock market. Today, we discuss the strong undercurrent in India’s services exports, which has the potential to transition the country from ‘Current Account Deficit (CAD)’ to a ‘Current Account Surplus(CAS)’, on a sustainable basis.

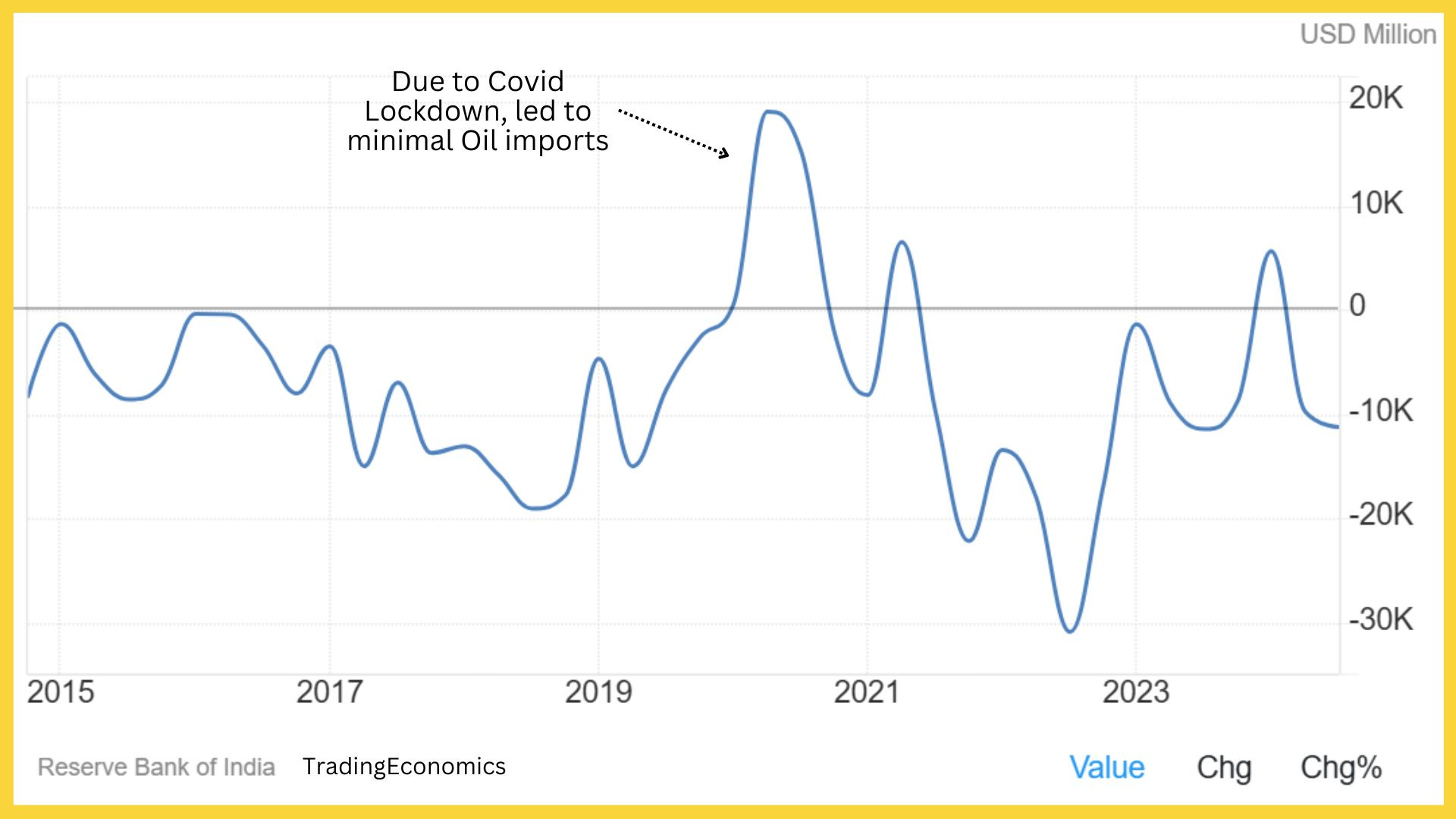

CAD occurs when a country's total imports of goods, services, and transfers exceed its total exports and transfers out, indicating a net outflow of dollars. India has long been in a deficit due to its high oil imports, as the country lacks domestic crude oil resources. India's gross oil import bill is projected to be approximately $140 Bn for the current year, given that nearly 90% of the country’s crude oil demand is met through imports. Back in 2015, Modi government had targeted to bring bring the import dependency on foreign produced crude oil to 67% by 2022 with 33% met via local production, but the reverse has happened with dependency actually increasing to ~90% today.

Over the last decade, the only full year in which India recorded a CAS was during the COVID-19 pandemic in 2020. With minimal movement and a sharp reduction in the oil import bill, India saw a surplus for the first time in decades as shown in the chart below⬇️

We are focusing on this because one key segment of the current account is signaling a major structural uptrend and has the potential to drive India into a sustainable surplus for the next decade: India’s Services Exports.

India today is where China was in 2000s

Since the onset of the 21st century, the biggest beneficiary of globalization has been China. Its annual exports have surged from $0.25 trillion in 2000 to $3.5 trillion today, making it a dominant player in global trade. Over the last 25 years, China's share of the global economy has risen by 13 percentage points, from 3.58% to 16.8%, and exports now account for approximately 20% of its GDP.

The table below illustrates how various countries' shares in global trade have evolved over time. In contrast to China’s meteoric rise, India's share has grown marginally by just 2 percentage points over the same period, currently standing at around 3.4% - roughly where China was 25 years ago.(Source)

Just as China revolutionized manufacturing exports, India today has the potential to replicate that success in services exports.

Rise of Indian Services Exports

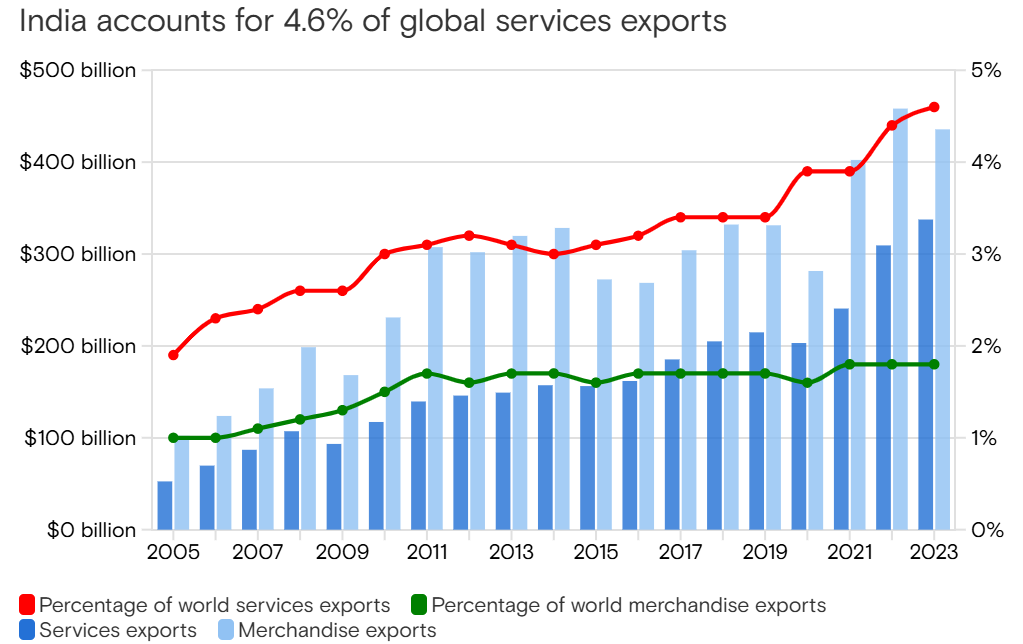

India today accounts for ~5% of global services exports against less than 2% share in global goods export. Services exports grew from $53 Bn to $338 Bn between 2005 and 2023 - almost double the rate of the rest of the world - and have come to form nearly a tenth of our national GDP. (Source: Goldman Sachs).

A significant portion of this growth has come from computer services (IT/BPM), which has consistently remained the dominant category in India’s services exports, accounting for 40% to 50% of total exports over the past two decades.

But now, things are evolving. While computer services continue to hold a significant share, the category - 'Professional Services' - is rapidly emerging. Also known as 'Global Capability Centers' (GCCs), these are offshore facilities set up by multinational corporations (MNCs) to manage various business functions, leveraging global talent, cost advantages, and operational efficiencies.

It is no longer just the IT segment being outsourced to India. Companies are now shifting core functions such as Operations, Finance, HR, Marketing, and Sales - classified under ‘Professional Services’ - to India.

Among organizations currently leveraging Global In-House Capabilities Centers (GCCs), 73% plan to increase their GCC investments in 2025. Additionally, 58% of organizations that have not yet adopted the GIC model are actively exploring its implementation.

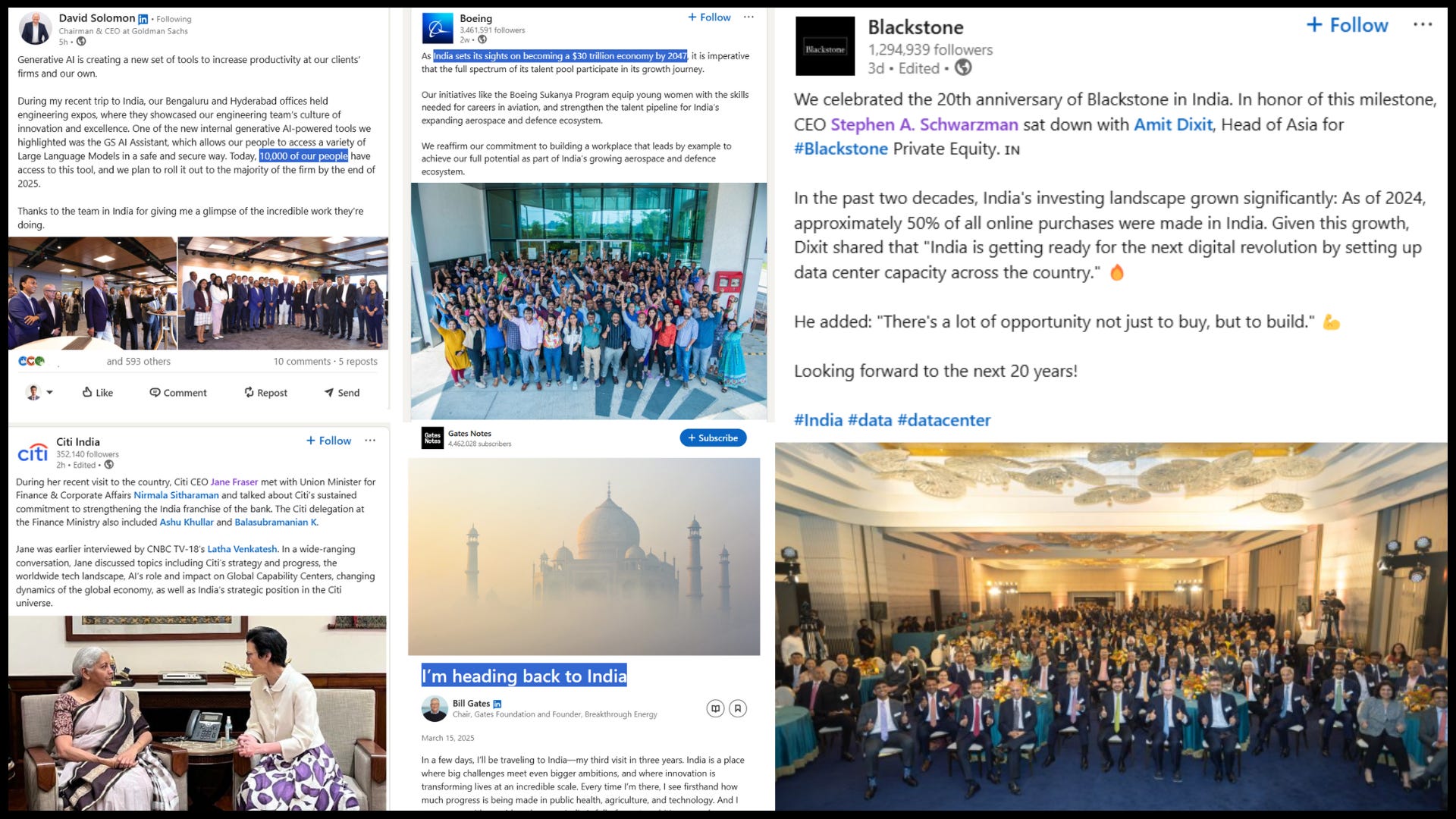

Below is a collage of global CEOs who visited India in March 2025 alone, reaffirming their commitment to invest and expand hiring in the years ahead. From Goldman Sachs to Citi, from Boeing to Blackstone, India has become a strategic hub for a majority of Fortune 500 companies today.

As per Goldman Sachs, the number of GCCs has more than doubled from 700 to 1,580 in last 20 years, and the sector has added around 1.3 Mn jobs, taking the total employee headcount to 1.7 Mn in the 2023 fiscal year. In a bull case scenario, they expect services exports would form 12.4% of India’s GDP by 2030 to a value of $900 Bn, which is more that double of what it is today in 2025. The Indian government estimates are even more bullish, expecting GCCs to expand to $105 Bn in terms of global services exports by 2030, employing over 2.8 million people, implying over 1.1 million new jobs in period of next 6 years!

But why would the world shift jobs to India?

The primary driver behind this shift is cost. Economies like the U.S. have long faced a labor shortage, which has only worsened post-COVID. As of January 2025, there are roughly 7.74 Mn job openings in the U.S. alone. Similar trend on shortage of skilled manpower is seen in Canada, Australia, and other developed markets, leading to rising wages as companies compete for talent.

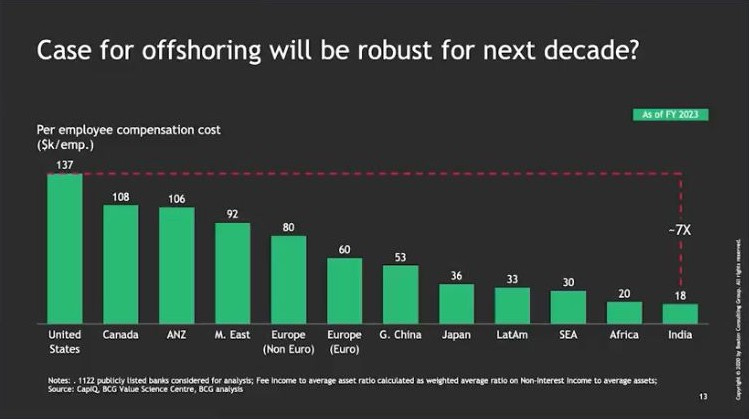

This cost arbitrage is pushing global companies to seek talent outside developed markets. In India, the same employee is available at just 1/7th of the cost in the U.S. as per a BCG slide shared below, with no significant differences in skill set, language proficiency, or technological adaptability.

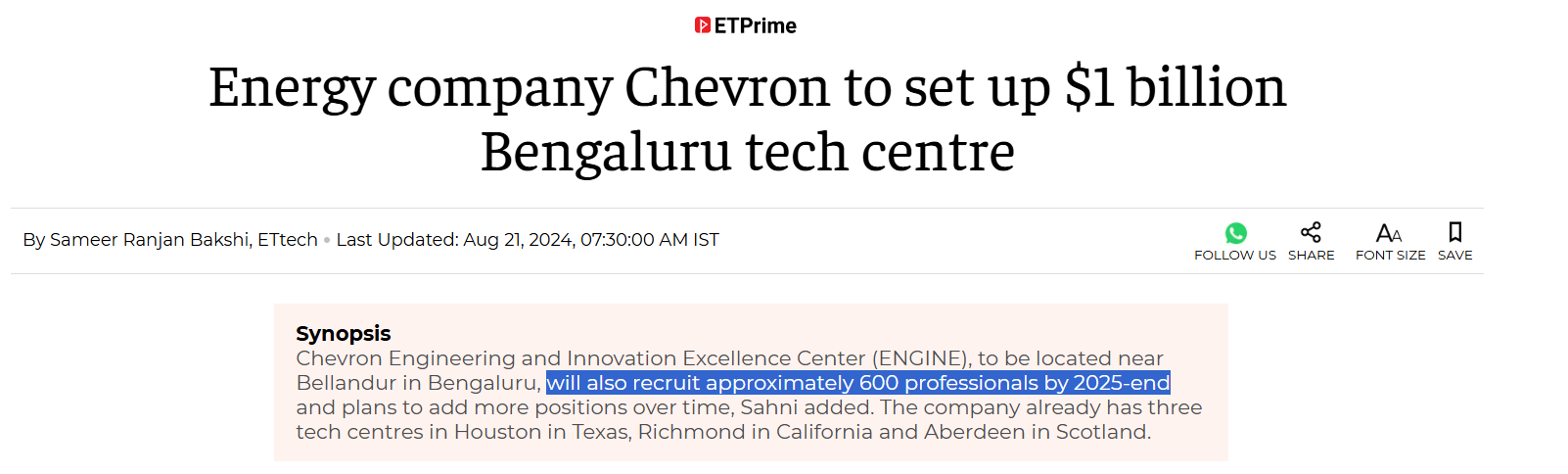

This cost difference is significant and enough to convince any global company like Chevron to setup their first office in India. Slowly overtime as they realize that it is working well, they expand & hire to offshore all their business operations to India.

For example, lets take case of Goldman Sachs:

In 2004, opened its first major office in Bengaluru, India

In 2014 started construction of a ‘Campus’ in Bengaluru, costing $250 Mn

In July 2021, opened a new office in Hyderabad, India

Today, has 10,000 employees in multiple divisions like technology, operations supporting global businesses

How much is India benefitting?

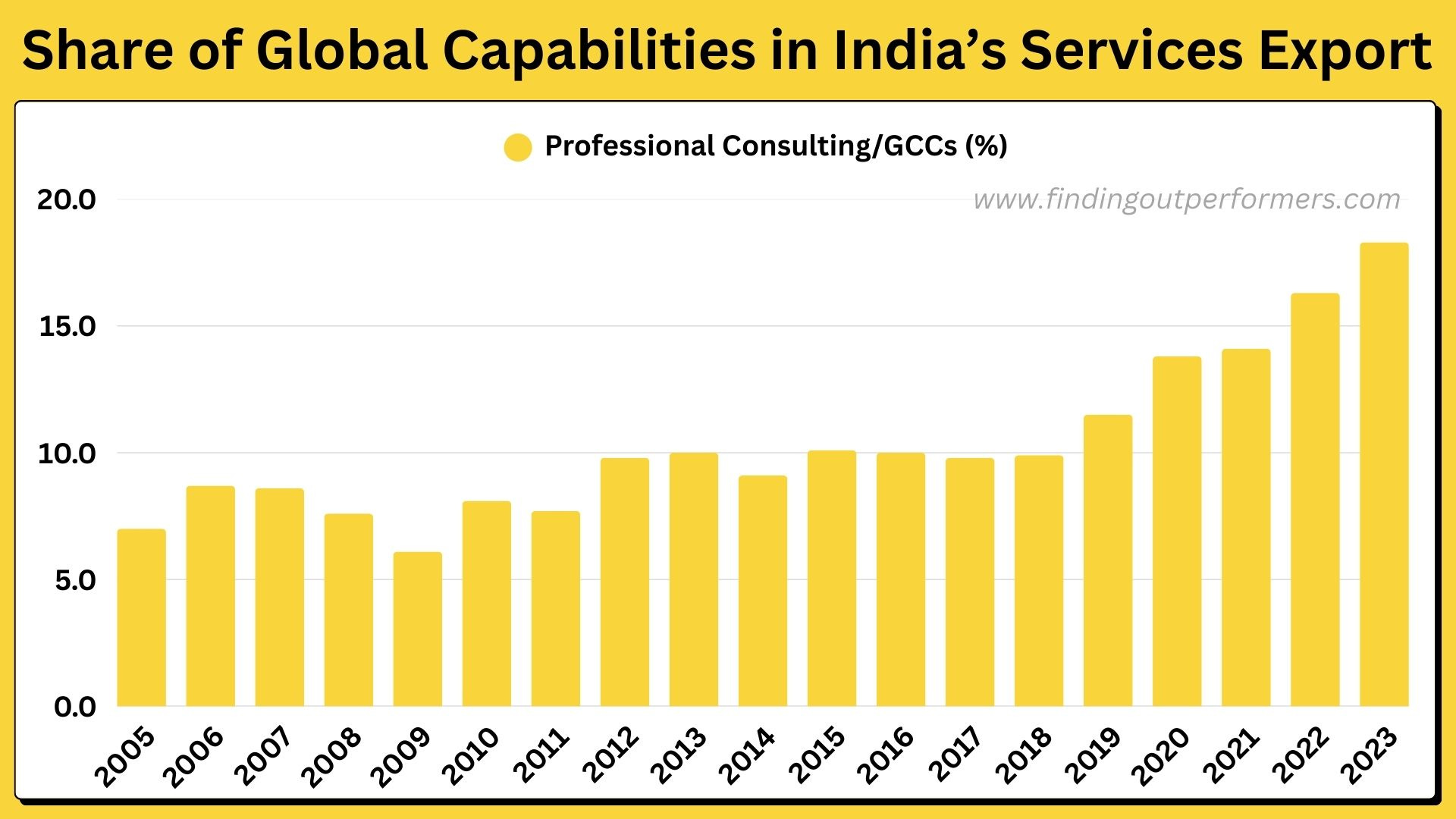

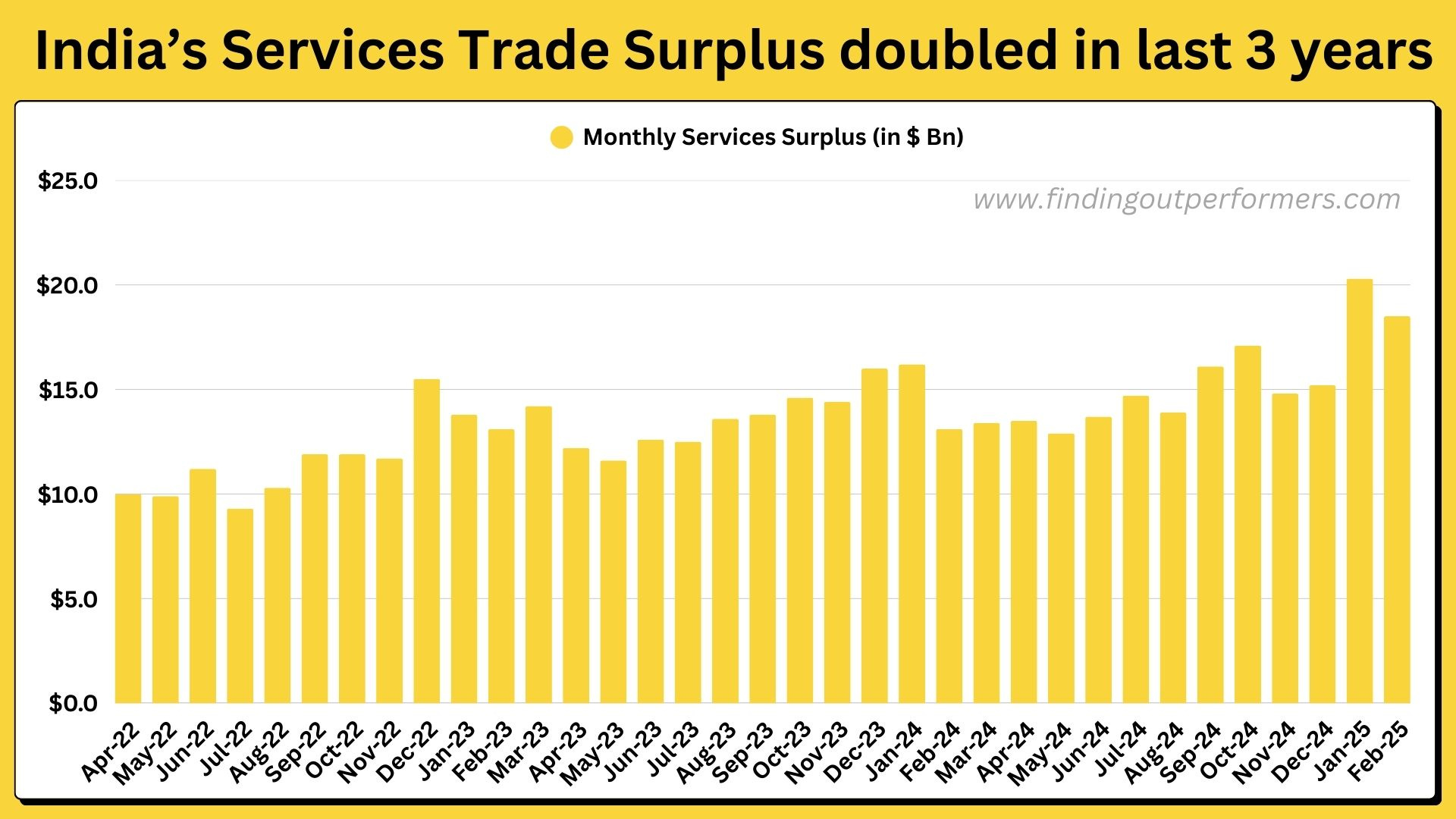

It's not just about jobs - it’s also about the foreign exchange inflows into India. The rise in services exports, driven by Professional Consulting/GCCs (whose share in India’s services exports has grown from 10% pre-COVID to ~20% today), has doubled the country’s monthly ‘Services Trade Surplus,’ now reaching a net inflow of $20 billion every month!

This is a significant boon for India, the world's second-largest crude oil importer, which spends $140 billion annually on oil imports.

If this monthly surplus of ~$20 Bn grows by another $10 Bn over the next two years, reaching ~$30 Bn per month, India would see an additional $120 Bn in dollar inflows annually. This could transform India into a ‘Current Account Surplus’ nation, with a surplus of about 2% of GDP - compared to the ‘Current Account Deficit’ of about 1% of GDP today - assuming other factors remain constant.

What gives us confidence of this surplus rising that fast?

COVID-19 proved that 'work from anywhere' is not only feasible but often just as efficient - whether from home, another office, or even another country. This realization has led companies to increasingly offshore key business verticals to countries like India, significantly reducing costs.

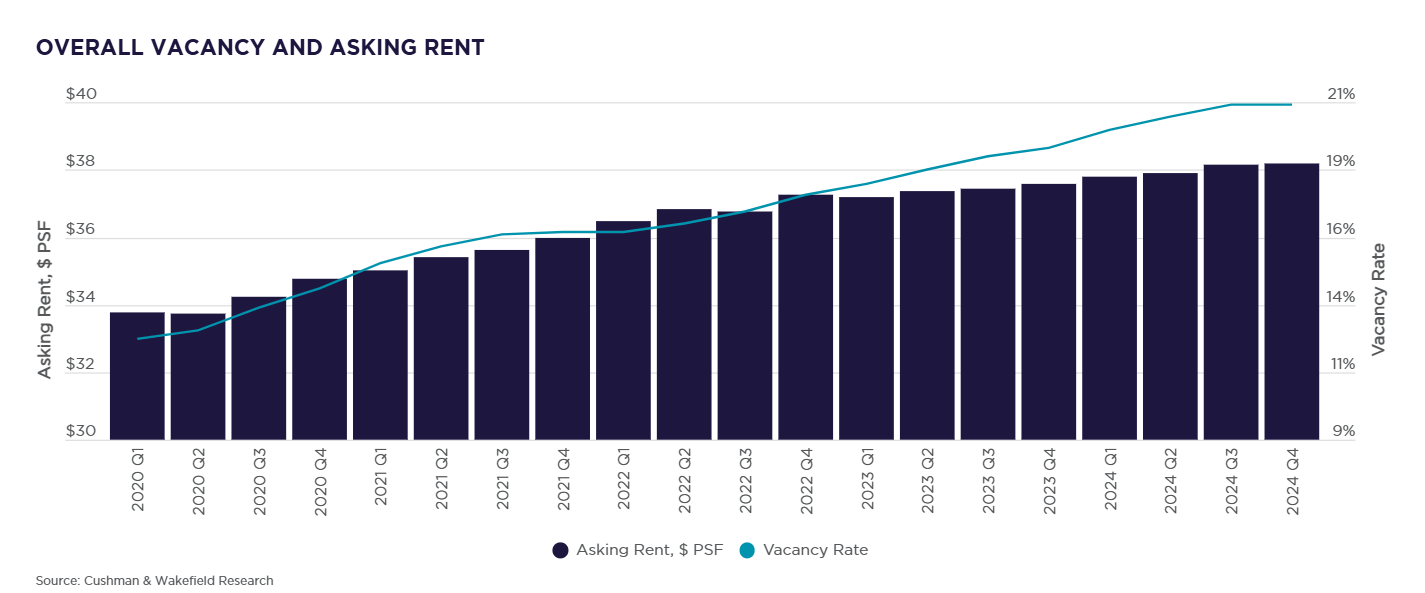

As a result, since COVID, the U.S. commercial real estate market has been in a downturn. Office vacancy rates have been rising every quarter, and today, nearly 20% of U.S. office spaces remain vacant, according as per Cushman & Wakefield.

While the U.S. commercial real estate market remains bearish, the scenario in India is the complete opposite. Global companies are struggling to find high-quality, large office spaces in major Indian cities, often having to wait several years before gaining possession of their bookings.

The chart below from Knight Frank illustrates how transaction volumes in India have been peaking since H2 2023. The number of deals far exceeds the actual completion of office spaces, indicating a growing backlog of excess demand.

With 35–40% of these transactions driven by Global Capability Centers (GCCs), it is increasingly clear that companies from the U.S. and Europe now see India as the ‘Office of the World,’ shifting more business functions and operations to their Indian offices.

Number of Forbes Global 2000 having a base in India is set to increase from 450+ today to 620+ by 2030, adding roughly 6 lakh new jobs.

Key Predictions

With the election year (2024) for India & USA behind us, with more businesses look towards India as their home, here are key expectation:

Momentum on shift of global operations by MNCs to India will gain further strength and surprise on upside. Exports from GCCs/Professional Consulting can cross the IT/BPM exports by 2035.

India’s Services Trade Surplus which hovers around $20 Bn monthly as we end FY25, could actually reach $30 Bn monthly by the time we end FY27.

India can become Current Account Surplus nation with 1% of GDP as surplus by FY27.

Indian Rupee can appreciate significantly and head towards ₹ 80/$ by FY27, reversing a multi decadal trend.

The above expectations are very away from what street expects the Indian currency to continue depreciating ~3% per annum which has been the long term trend.

Key Risks

Multiple reasons could prove us wrong:

Tariff war on global trade (primarily goods trade) create an environment of uncertainty, making it hard to predict what could be next move coming from US President.

Inflation in India must remain under control like it is currently at start of 2025, hoping better rains to keep food inflation under control.

Global wars continuing/start of new war in various parts add to major uncertainty.

Moment of Dollar index would partially impact currency move.

AI could emerge as a risk for IT, but we don’t expect a severe impact on trade surplus of the same

Any new risks or amplifications of existing risks that are unknown today but could emerge later.

TO END: We hope you enjoyed this comprehensive analysis on this structural shift happening for India making us even more bullish on the country’s long term growth trajectory. Stay tuned for Part 2!

Connect with us on LinkedIn here: Yash Agarwal and Aditya Grover

If you liked our work, consider supporting us at Finding Outperformers by contributing here:

Read our previous blog:

Disclaimers-

We are not a SEBI registered advisors; personal investment/interest in shares can exists for any company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the decision maker is responsible for any outcome.

| A guest post by

|