Did the elephant fall while dancing?

Part 1: Discussing why HDFC might be in a tough situation in the near term

Recently India’s largest bank by market cap, HDFC Bank, lost INR 1.3 lakh crores in market cap in just 1 week of announcing its Dec ’23 results. It’s one of the bank’s biggest falls it witnessed since getting listed in 1995. As I begin to write this blog, I must declare that I don’t own any share of HDFC bank - nor in my portfolio, nor do any of my family portfolios own it as of today. There was a time 2 years back when ‘HDFC Bank + HDFC Ltd’ made 20% of my family’s total equity portfolio, but it’s been cut down to 0% now over this period of 2-years. I don’t plan to add it to my portfolio even after the dip we have seen post Q3 FY24 results as I am yet not confident that HDFC bank will get its Mojo back soon. Hence now, I’m biased for not owning it, and shall be giving you my thesis of not having HDFC Bank in my portfolio, from a Short and Medium-term prospective.

It’s getting messier before it gets better!

Let me bring your attention to how our banking system has fared in the aftermath of the COVID-19 pandemic. Focusing on the fundamental functions of banking, namely giving loans (credit) and taking deposits, I have included a graph illustrating the growth of credit and deposits in India.

Starting with credit, immediately after the pandemic, there was a two-year period of subdued growth. We remained below a 10% credit growth rate in India, despite a record low-interest-rate environment, until April 2022. Then, after exactly two years, we finally surpassed the 10% range due to a boost in economic activity, driven by a lower base and positive sentiment. From July 2023 onwards, the merger of HDFC Ltd (formerly an NBFC) with HDFC Bank contributed ticked the 'banking' credit growth rate even higher. Adjusting for HDFC Ltd, the credit growth has been around 15-16% in the second half of 2023.

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 1K+ monthly readers!

The deposit side of the banking system has also seen growth, albeit at a slower and consistent pace, averaging a 10-11% Compound Annual Growth Rate (CAGR) in the post-COVID period. This rate has increased to an average of ~13% in the second half of 2023, thanks majorly to a lower base, and to some extent, HDFC Ltd’s deposits now added to the total banking deposits.

However, this has created a noticeable gap in the rate of growth between credit and deposits, amounting to an average of ~3% over the last two years. Sustaining this gap in the medium to long run is challenging because banks heavily rely on the amount deposited by individuals as a major source of liquidity.

Therefore, in the next 1 to 2 years, either deposits will need to increase faster or credit growth needs to slow down. As of December 29, 2023, credit growth stood at 20% Year-on-Year (YoY), and deposits rose at 13.2% YoY, reaching ₹159.6 lakh crore and ₹200.8 lakh crore, respectively. When adjusted for the HDFC-HDFC Bank merger, credit growth stands at 15.7% YoY, and deposit growth stands at 12.6% YoY.

Where has the Liquidity gone?

Let's turn our attention to another crucial data point—the overall liquidity in the banking system, a factor largely controlled by the central bank through its interactions with commercial banks. When the central bank aims to stimulate economic activity by enhancing financial liquidity, it employs various tools to increase liquidity with the banks. This was particularly evident during the COVID-19 phase when the central bank actively worked to support and boost economic activity in India. Liquidity is also affected by cash use in the economy. More the cash we withdraw from the bank, the lesser the liquidity with the banking system and vice-verse.

As of the beginning of 2024, the liquidity in the banking system is in a deficit of over Rs 2 lakh crores. This marks the highest deficit in the last eight years, attributing to the signaling a tightening stance and the withdrawal of liquidity from the system by the Reserve Bank of India (RBI), lesser government spend and greater cash withdrawal by public. In the graph provided below, a figure above '0' indicates a deficit in the system, while a figure below '0' suggests excess liquidity within the banks to support economic buoyancy.

The current deficit in overall banking system liquidity may not have a direct impact on the banks' ability to grow their credit, but it does exert an indirect influence. The tightening of liquidity can negatively impact the overall system's ability to extend credit over the medium term. It's important to note that the Reserve Bank of India (RBI) has substantial control over this situation and can bring it back to surplus when deemed appropriate.

However, if this liquidity deficit persists alongside the existing gap between credit and deposit differentials, banks may face challenges ahead. This situation could potentially lead to an increase in their cost of borrowing, adding another layer of complexity to the banking landscape. Monitoring this situation will be crucial.

To bolster my case for the importance of securing more deposits, consider the recent interview with the RBI Governor on CNBC with Shereen. This conversation took place in the aftermath of HDFC Bank's significant decline following its financial results. In the interview, the Governor explicitly emphasized the necessity of a 'correlation' between credit growth and deposit growth for all banks. He cautioned against excessive enthusiasm for lending, highlighting the need for a balanced approach. For further details, I recommend watching the interview clip starting from the 7:17-minute mark to 10:50 minutes:

These remarks of the RBI governor are coming after the whispers which recently came out in the market that RBI is not comfortable with ‘Credit to Deposit’ (CD) ratio of some banks in India. “There is no specific number for the CD ratio given to the banks by the Reserve Bank, but 70-80% is its comfortable range,” a source told FE.

For understanding: The ‘Credit to Deposit’ (CD) ratio measures how much a bank lends out of deposits it raises. For example, a CD ratio of 75% means that three-fourths of deposits have been given out as loans.

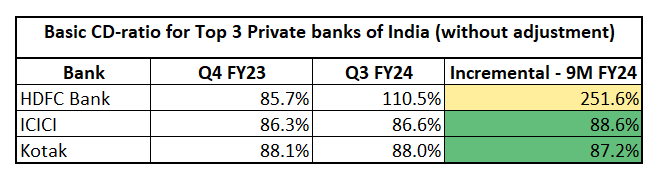

Considering this ratio is gaining importance for RBI who is looking to have a close watch over it for all banks, we decided to calculate the basic form of ‘Credit to Deposit’ ratio (without adjustments) for top 3 private banks in India: HDFC Bank, ICICI, and Kotak. In this exercise, we simply take the total credit and deposits figures mentioned by them in their investor presentation for these 2 quarters: Q4 of FY23 and Q3 of FY24 - from which we calculate the incremental CD-ratio for the banks over the 9 months from April to December of 2023:

The highlight of this table is HDFC Bank because its CD-ratio is increased significantly from 85.7% to 110.5%, all because of its merger with HDFC ltd which had a large credit book but only a small portion of their book was funded by customer deposit, as is usually the case with any NBFC. The key reason I am bringing up this table here is that HDFC bank will have to:

Bring back the CD-ratio to pre-merger levels

Will have to pursue ‘Point 1’ faster now since sense is that RBI can get more stringent when it comes to CD-ratio

Hence they will have to push for deposit growth much harder at a time when there is still exists a 3% differential in the credit and deposit growth rate at the systemic level and Deposits have grown at a slow ~11% CAGR over last 3 year.

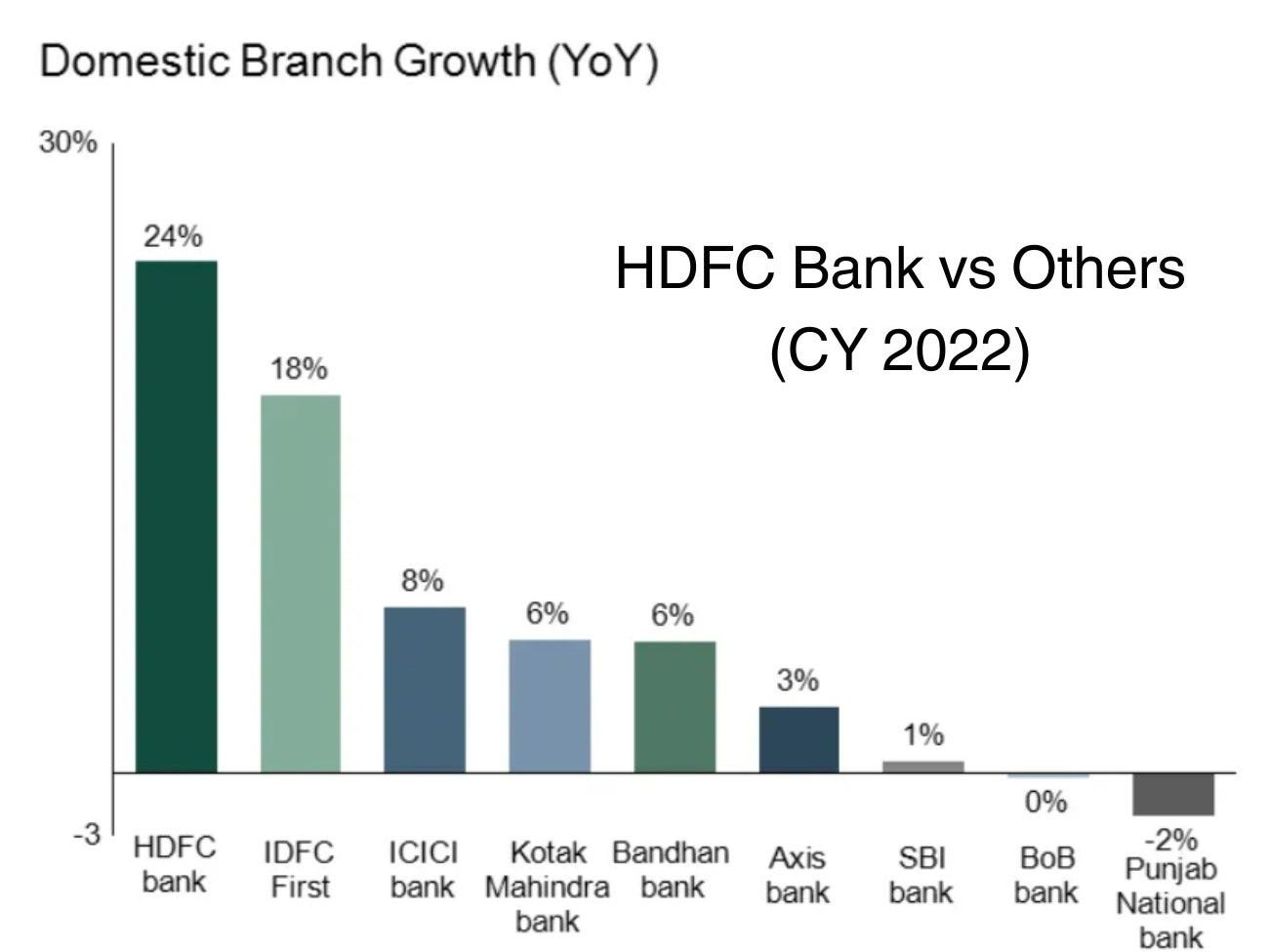

But HDFC bank isn’t caught off-guard in this situation as they were preparing for the need of higher future deposit growth branch even before the merger happened:

In 2022 alone, HDFC bank alone opened about 1400 branches which was about 70% of the total ~2000 branches added by all major banks in the system in that year; simply HUGE!

In 2023, the pace of branch opening has moderated to total ~900 branches by the bank, but the management has guided for many more branches in future as they target to have a branch within 1-2km radius of their customer.

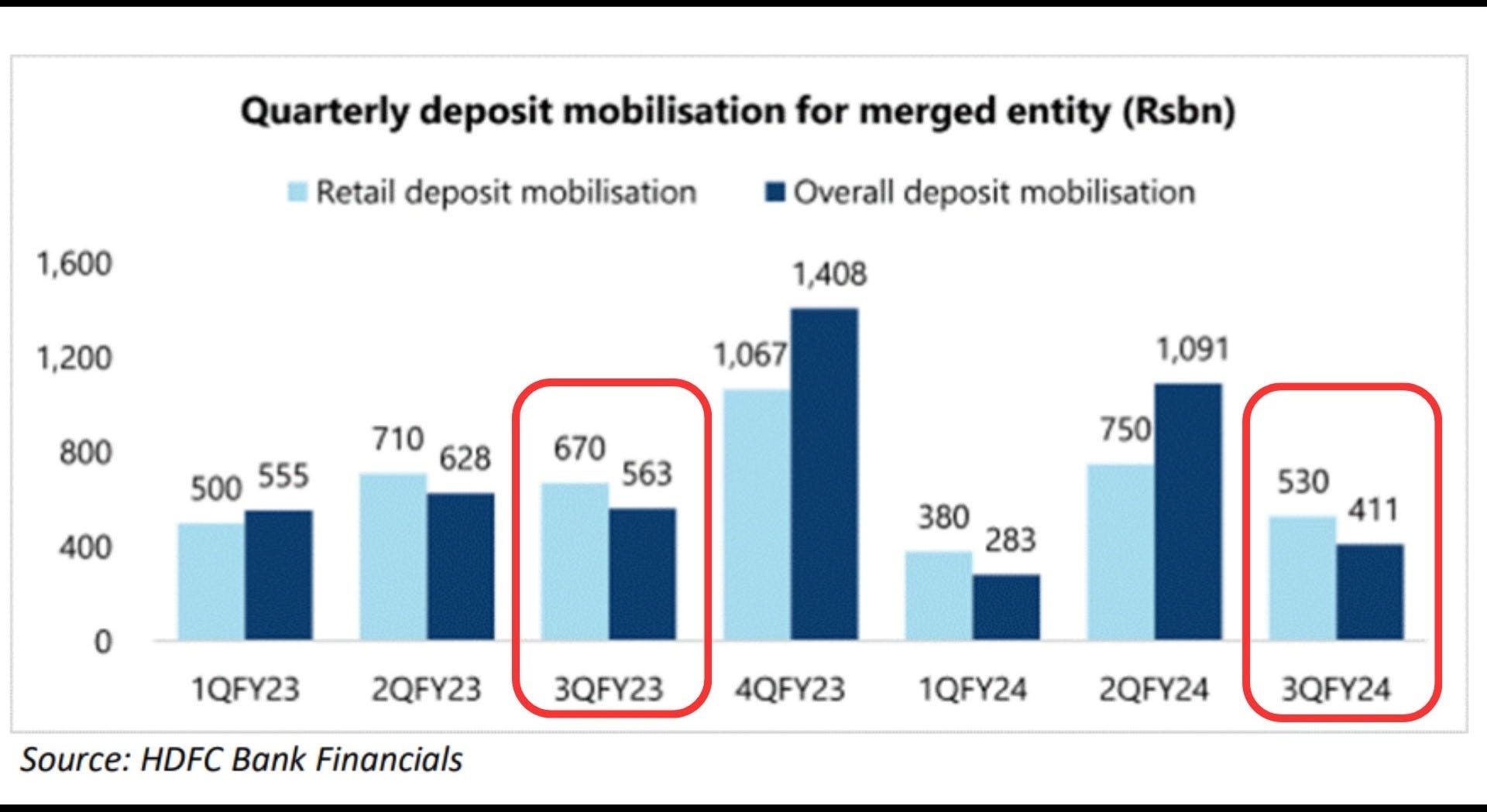

The outcome of this is visible in the Dec’2023 quarter, where the ‘Deposit’ for HDFC Bank (on standalone basis) grew a healthy ~22% YoY. On face it, it look goods, but the devil lies in details. The thing that street has not liked about results is that the quantum of deposit garnered in Q3 FY24 is actually lower than what they got last year in Q3 FY23. Considering the number of new branches opened, which is roughly 25% of their total branches today opened in just last 2 years, one would have genuinely expected a higher number:

Fears are Growing, when will NIMs compression end?

Out of the 3 top private banks of India: HDFC, ICICI, & Kotak - ICICI Bank has been able to grow its deposits at fastest rate in Q3 FY24 on QoQ basis at 2.9% where as both HDFC Bank and Kotak Mahindra Bank stood at 1.9%. But this ‘Rank 1’ for ICICI has come at a significant cost: Net Interest Margins (NIMs) compression. It’s NIMs have compressed by 10 basis points in this quarter and cost of deposit have risen by 19 basis points in just single quarter.

Now this is big trouble opening. At a time when market is expecting HDFC Bank to improve its NIMs steadily over coming quarters, a rising cost of deposits at this stage of interest rate cycle in the system means that journey can be a tough one ahead. If the 2nd biggest private player in the market is willing to sacrifice margins in order to grow deposits faster, it implies that journey for the 1st biggest private player, who has planned and now obliged to raise the deposits at a much faster rate to bring down its CD ratio at accelerated pace, is now going to be tough.

To Summarize:

It will be very important for HDFC Bank to improve their margins in coming quarters and at no cost can they allow their margins to stay stable or compress. If they margin profile doesn’t improve, it opens the room for more disappointment for the street and the might not be able to produce good returns for its shareholders. Though this isn’t an investment advice, but it will be interesting to see when will the elephant get back to dancing again. Let me know your thoughts in the comments. Thankyou for reading till here and I hope you find this blog useful.

Find me on LinkedIn here.

(Thanks to Priyansh Chanchani for helping me out in writing this blog post)

Consider sharing with your friends. If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 1K+ monthly readers!

Disclaimers-

We are not SEBI registered advisors; personal investment/interest in the shares exists for the company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome.

I think the culprit is recent C/D ratio. HDFC Bank should have been more vigilant on this.