Has IDFC First lost the plot?

A writeup on why I sold my holding after 5 years

I first learned about IDFC First Bank in December 2019 when one of my college professors mentioned it during a lecture. He spoke about the founder’s journey from Capital First and how it merged with IDFC Bank in 2018 hence obtaining a banking license, among other things. The story was interesting, but I only researched more about it once Covid struck and the country went into a complete lockdown. I then had many discussions with my dad, and by June 2020, the bank had become the largest holding in our portfolio. Over the last five years, I was also fortunate to connect with the founder himself through my research, which he appreciated.

Fast forward to today, as I write this blog, I have decided to exit the stock. I have sold the majority of my holding of the bank recently and plan to sell the remaining soon. It was a difficult decision, filled with doubts about being wrong, but I will try to justify why I made this call after closely following the company for many years.

Before we begin today’s blog, I’d like to welcome the ~500 new subscribers who have joined us in the past month since our Zomato’s Social Ads blog. We now have around 4,000 subscribers, and it’s great to have you all here as we continue our journey to find the next potential outperformer. Activity on this blog website has slowed down a bit due to certain professional commitments, but I’m hopeful of keeping it going with even more momentum in the future.

Let’s get started!

Jan 2023

About two years ago, I shared an extremely bullish view on IDFC First Bank, which can be read here. In that piece, we discussed why the bank had the potential to outperform other banking stocks over the year.

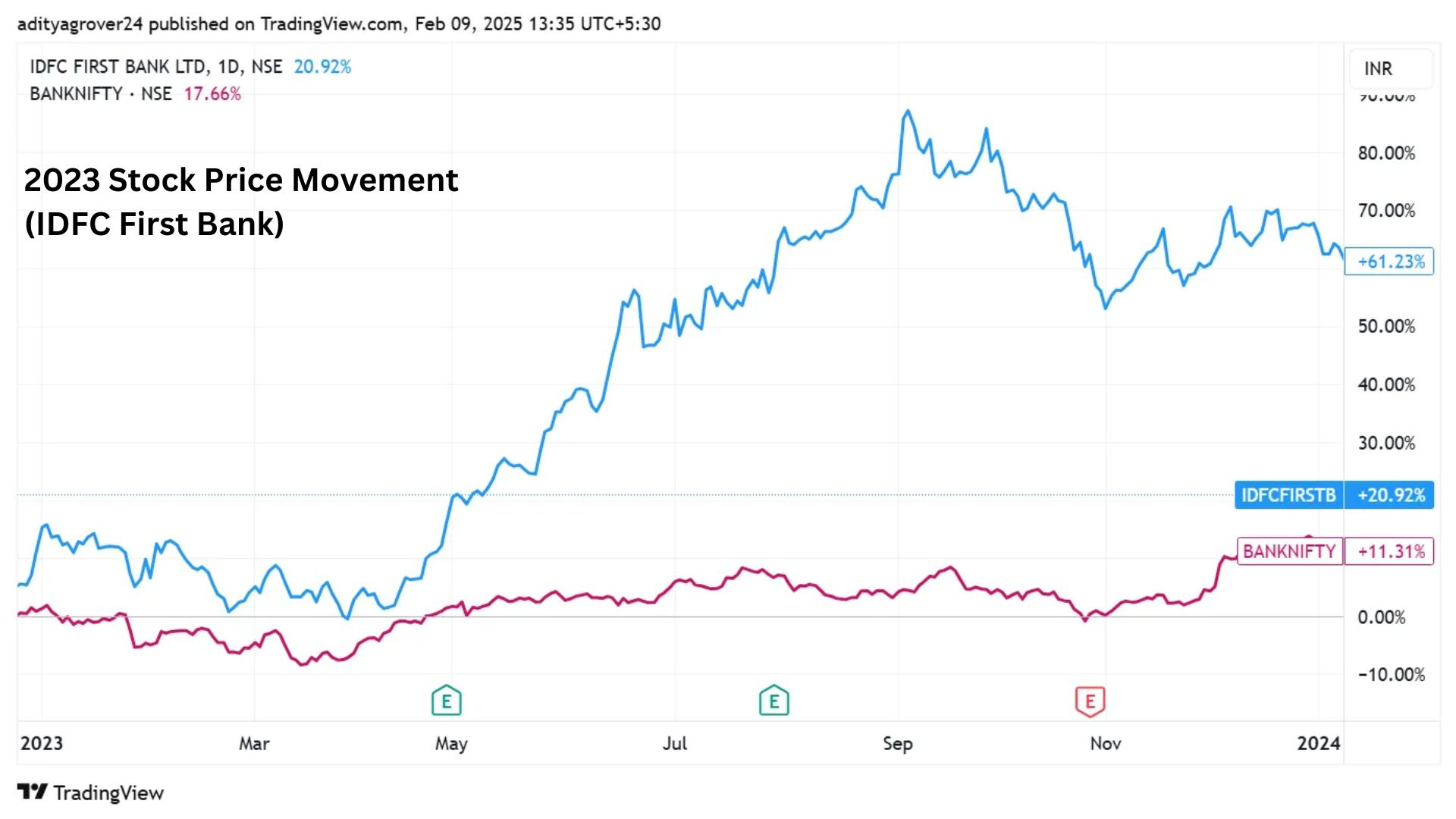

Thankfully, 2023 played out along similar lines, with the stock rising ~60% during the year compared to Bank Nifty’s ~11% return, as shown in the 2023 chart below:

But 2024 didn’t turn out well for the stock. With retail participation peaking, it delivered a negative return of 25% for the year.

I didn’t publish any follow-up blog on the company after that, as my focus shifted to my current main holdings, including Zomato, Tata Power, DLF, PB Fintech, IHCL, and more. However, as I exit my position, I wanted to share my thoughts. I won’t discuss valuations or other technical aspects (which I rarely do anyway) but will focus more on the soft factors that led me to this decision.

Doubt on Profitability Prospects

“FY2023-24 should be better than '23, '25 should be better than '24, '26 should be better than '25, that is something you should expect from us”

- V Vaidyanathan, CEO & MD (July, 2023)

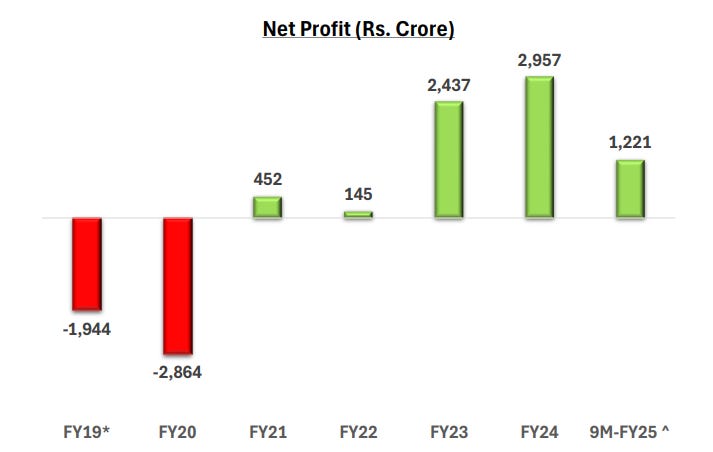

The bank had a strong turnaround post-Covid, delivering solid profits in FY23 and FY24. However, that momentum now seems to have stalled. It is often said that in banking, real underlying risks can be easily hidden beneath the surface - I anticipate that could be the case here as well.

The company has struggled to meet its profit growth guidance due to several issues, including a high cost-to-income ratio, NIM compression, and more. A recent hit to profitability has come from issues in its microfinance loan book, where asset quality has suddenly deteriorated. At the end of 2023, this segment accounted for ~7% of the bank’s total loan book, but it has now declined to below 5% by the end of 2024.

Cracks are visible & getting deeper

“Microfinance business was an amazing silver bullet, which met 3 requirements …. we were lending at ~ 24%, we had some additional fees on top of it, our cost of funds was really nothing like 6% or 7%, and it just made a lot of money.”

- V Vaidyanathan, CEO & Founder (Jan ‘25)

Sweet grapes turned sour very quickly for the bank. The credit cost (which includes write-offs and provisions against that part of loan book) for IDFC First’s microfinance portfolio was just 1.6% in 2022 and 2023. However, in 2024, it has suddenly surged to ~10%, indicating that a significant portion of the loan book would never be recovered now.

The management has warned that the worst of the sector's pain is expected to peak in the Jan–March '25 period, suggesting this 10% figure could climb even higher.

Alongside, the recent development in Karnataka can’t be ignored.

Recently, on February 12, 2025, the Karnataka government issued a notification to enforce a new law regulating the microfinance sector in the state. The law includes strict penal provisions, such as imprisonment of up to 10 years and a fine of ₹5 lakh for violations by agents. This ordinance was introduced following multiple suicide cases linked to coercive recovery tactics, including criminal intimidation by moneylenders. While the intent behind the law is justified, its impact on the sector will be significant, as many borrowers may now choose not to repay their small loans, given the limited recovery powers left in the hands of microfinance lenders.

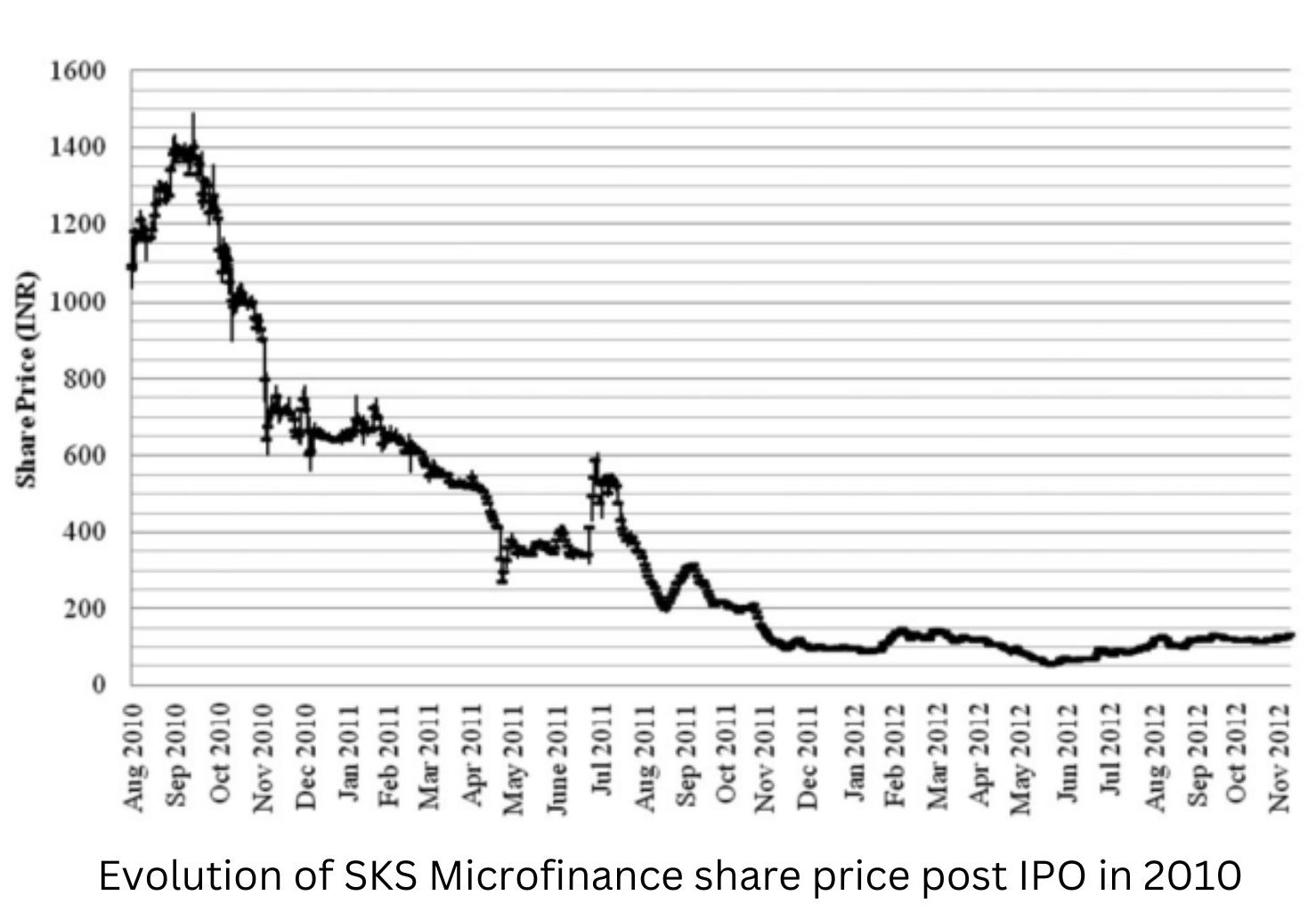

A similar situation occurred in Andhra Pradesh about 15 years ago when the state government introduced laws to protect borrowers.

On October 14, 2010, the Andhra Pradesh government announced an ordinance to curb ‘harassment’ by collection agents—much like what is happening in Karnataka today. In response, many rural financing companies, including SKS Microfinance and other MFIs, decided to cut interest rates. However, this move backfired as it highlighted the already widely criticized high interest rates, reportedly between 24% and 28% annually - a range that, as per V. Vaidyanathan’s statement, remains unchanged even today.

The rate cuts also exposed the fact that lower interest rates were feasible all along, but MFIs (Microfinance institutions) had been unwilling to offer them.

Politicians began attacking the microfinance sector, urging those living in poverty not to repay their loans. As a result, SKS was forced to write off 90% of its loans in Andhra Pradesh and lay off 10,000 employees.

“When the crisis broke out in October 2010, we had ₹ 1,430 crore exposure in AP. We collected some ₹ 129 crore. So we had to provide for about ₹ 1,300 crore. We did that over seven quarters so that it doesn’t ignite a crisis of confidence.”

- S. Dilli Raj, CFO, SKS Microfinance, 2013 (Source - click here)

Now, with a similar situation unfolding in Karnataka, the worst for the sector may still be ahead. This crisis could easily spill over to neighboring South Indian states and other regions where governments are actively seeking populist measures to win public support.

Additionally, the microfinance turmoil could extend to other rural-focused or high-interest loan segments, including rural finance and consumer durable loans within the state. IDFC First has a 9% exposure of its loan book to Karnataka as of Dec ’24.

“The credit discipline in Andhra Pradesh has been wiped out and the biggest task is to bring it back”

- S. Dilli Raj, 2013

Are we presenting the data correctly?

Shifting focus to how the company presents data in its investor presentation - something I’ve recently started analyzing more critically.

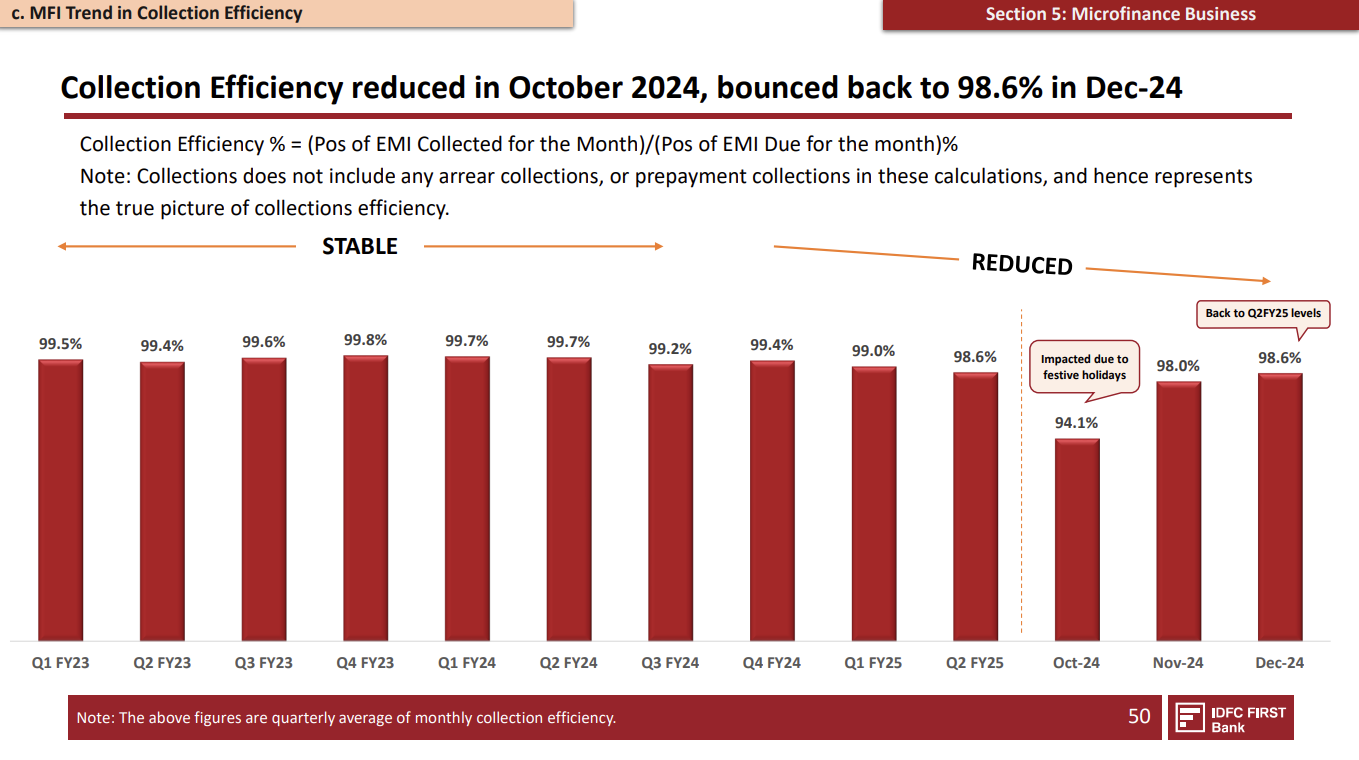

For context, the bank’s microfinance loan book has declined by 20%, from ~₹13.6K crore in 2023 to ₹11K crore in 2024, primarily due to write-offs and controlled loan disbursals to the sector. In its investor presentation, the company reports ‘collection efficiency’ for each month of 2024. However, it does not account for loans that were either written off or had provisions made against them during the quarter. Instead, it chooses to display collections only from healthy loans, thereby reflecting a high collection efficiency of 98.6% at year-end - even at a time when the sector is under severe stress.

In reality, the bank’s microfinance loan book shrank by about ₹1,500 crore in Q3 FY25 alone which is 10%+ of their loan book to that sector, with a significant portion of the decline driven by write-offs.

Had the company presented the collection efficiency by including all loans (both healthy and written-off) in the denominator and actual collections in the numerator, the percentage would have dropped sharply - providing a more accurate & better representation of the true picture, in my view.

In other words, I believe the company has the discretion to decide what data to present and how to present it to investors. However, I would have expected them to act more transparently in this case. It makes little sense to showcase such data merely to reassure investors that everything is fine when, in reality, that may not be the case. This isn’t just a one-off case; I have been getting this sense over time after tracking them for years.

After Microfinance, what could crack next?

As of December 2021, the bank’s retail loans stood at around ₹87,000 crore, growing to ₹187,000 crore by December 2024. This implies that the majority of the bank’s loan book has been disbursed within the last three years, in line with management's guidance.

However, what concerns me is the possibility of stress emerging in other parts of the loan book, just as it did with microfinance. In most downcycles, the microfinance segment is typically the first to witness defaults, and this has the potential to spill over into other loan categories - which is worrisome.

In banking, where evergreening is common and real stress is often concealed, it can take years for bad loans to surface. While I still don’t believe IDFC First Bank is actively engaging in such manipulative practices, my confidence has eroded over time - especially given how they chose to present data in the case of microfinance.

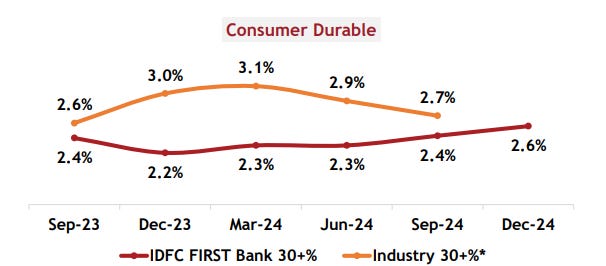

For instance, let’s look at the NPA percentage in the bank’s consumer durable loan book:

This is another high-risk, high-reward financing category in which the bank is actively involved, with ~4% of its loan book allocated to it.

The NPA levels in this segment are now almost on par with industry averages (including both banks and NBFCs), indicating the level of risk the bank may have taken to expand its loan book in this category over the past 2–3 years. This raises concerns about the stability of this growth and casts doubts in my mind about its foundation. In fact, the credit cost for their loan book (ex-microfinance) have already been on an uptrend from 1.7% in Q1, to 1.8% in Q2 to ~1.85% in Q3 of FY25.

Is the Margin party over?

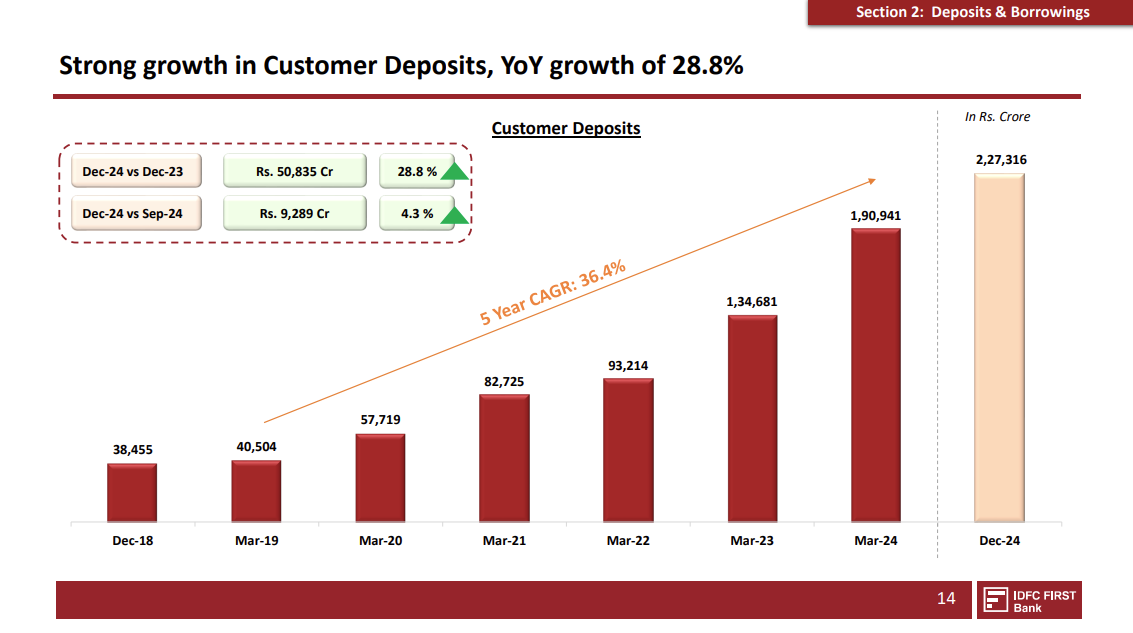

IDFC First has enjoyed very healthy net interest margins (NIMs) of over 6% in past many quarters. Over the past year, as the RBI tightened regulations, banks with a high Loan-to-Deposit (LTD) ratio were instructed to raise deposits more aggressively to bring the ratio down - I had written about this more than a year ago here. Among the most impacted were banks like HDFC Bank and IDFC First. However, IDFC First has done an impressive job in growing its customer deposits. The bank expanded its branch network aggressively post-Covid, now reaching ~1,000 branches. Additionally, its digital strategy, particularly its mobile app, has been highly effective in driving growth.

One major factor contributing to the growth in deposits is the high interest rates IDFC First Bank offers on savings accounts. While Axis Bank offers around 3–3.5%, IDFC First provides a significantly higher ~7.25% on deposits above ₹5 lakh.

These customer deposits also helped the bank repay its legacy infrastructure bonds, which were issued by the pre-merger entity at higher rates. This, in turn, supported the bank’s margins (NIMs). However, that advantage no longer exists, as most of these bonds have now been repaid.

With emerging challenges in the microfinance segment and other high-margin products, further margin compression is highly likely, casting a shadow over the bank’s profitability prospects further. And if they reduce the saving rates in coming months, I wonder if they will be able to sustain the growth momentum in deposits anymore.

“The reason why the income will not grow directly in proportion next year is that the microfinance, like I said, is a highly profitable business. We were lending at 24% rate (but that loan book is expected to further reduce taking away that margin advantage)”

- V Vaidyanathan, CEO & Founder (Jan ‘25)

Yet another fund raise needed!

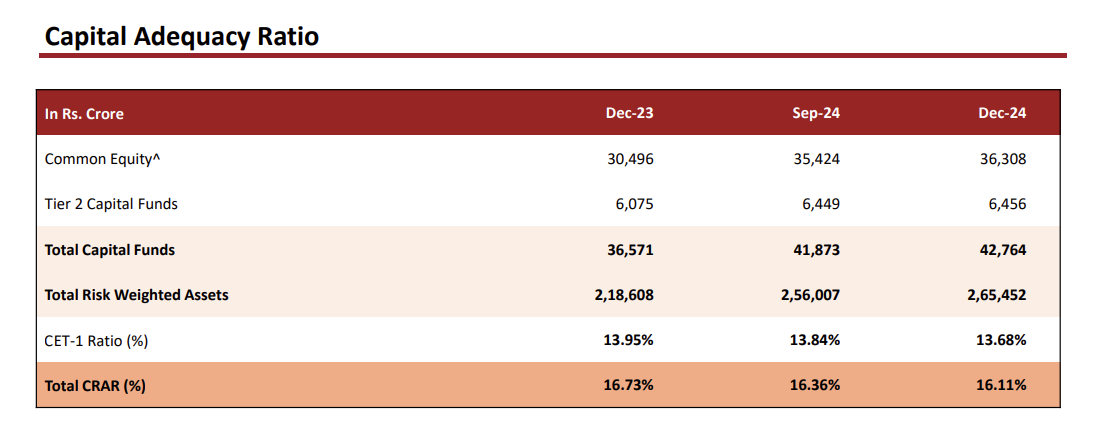

The bank has been consistently raising funds, with the most recent being a ₹3,200 crore preferential issue to mutual fund houses in July 2024. But despite all fund raises, its Capital Adequacy Ratio (CAR) stands at 13.68%, which, while above the regulatory requirement, indicates the need for another fundraise.

While the RBI mandates a minimum Capital to Risk-Weighted Assets Ratio (CRAR) of 11.50% for banks in India, IDFC First Bank currently stands at 16.11% on this parameter. However, this is still significantly lower than other large private banks that IDFC First aspires to compete with, making additional equity infusion highly likely to enhance the bank’s financial stability and investor confidence.

This suggests that IDFC First Bank will likely undertake another round of equity dilution in the near future. While this may strengthen the bank’s capital base, it is a negative for existing shareholders as it reduces their stake and share in future profitability.

Good Bye, IDFC First!

The reasons I focused on today are primarily driven by how issues in the microfinance loan book have significantly impacted profitability and led to margin compression. The way this unfolded over the past year raises concerns about the quality of the loan book, and the way it was presented in investor communications has been disappointing. If a similar issue arises in another segment of the loan book - which I now anticipate - it could become a nightmare for investors, especially retail investors, who hold a substantial portion of the stock.

Additionally, on a broader level, I am not particularly optimistic about the banking sector as a whole. I strongly believe its weight in the index should decline over time, with technology stocks taking the lead instead. That’s where I’d prefer to shift my focus going forward.

So, it’s goodbye to IDFC First - for now! Connect with me on LinkedIn here.

Finding Outperformers is a free-to-access website, and your support shall help us keep going.

Disclaimers-

We are not a SEBI registered advisors; personal investment/interest in the shares exists for the company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the decision maker is responsible for any outcome.

Thanks Aditya for sharing your thoughts . Concise , Precise and Candid . I have been holding IDFC for long . Just betting on Vaidyanathan sir .Taking back the capital and will keep the profit invested .As of now will continue to HOLD

Whoa! great piece. Loved the fact u focussed on the story and soft issues rather than marinating us in numbers as most other analysts and news pieces tend to do.

Keep writing!