Is Bank Nifty losing its charm?

Many research houses turn relatively bearish than before....

Hello there! I'm here to discuss a pressing issue in the Indian stock markets – the recent underperformance of Banking stocks. Notably, major banks like HDFC, SBI, and Kotak Mahindra Bank have been experiencing significant underperformance.

Some of this can be attributed to specific factors affecting individual banks. For instance, HDFC Bank might be facing adjustments in institutional holdings due to its merger with HDFC Ltd. Similarly, Kotak Mahindra Bank shareholders may be seeking clarity regarding the bank's succession plans.

In the past three months, the Bank Nifty index has notably lagged behind the Nifty 50 index by around 4.5%. You can see this trend in the chart below, where the yellow line represents the Nifty 50 and the other line represents the Bank Nifty.

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 400+ readers!

Even equity researchers in various fund houses have come out with their banking reports showcasing caution. In just the last 10 days, several big fund houses turned cautious over banks. I went through 4 foreign houses’ reports: Jefferies, JP Morgan, HSBC & BofA, before writing this blog to understand their perspective and which all banks they think would perform better than the others; LET’S GET STARTED!

What’s the biggest worrying factor?

The answer is Net Interest Margins (NIMs)!

NIMs is the difference in the rate at which banks borrow money from people in the form of deposits and lend it further as loans. It is now the 'show stopper' for all results! To understand NIMs in a simpler way, here’s a formula (not exactly correct):

NIMs = Interest rate on loans - Interest rate on deposits

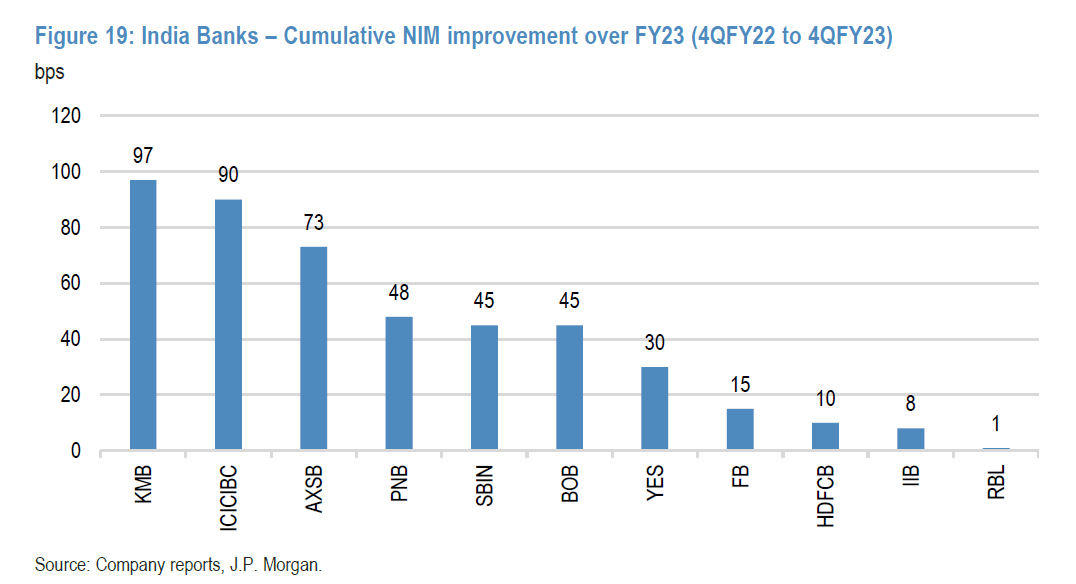

Post RBI raising rates over the last 1-1.5 years, banks have been forced to increase their lending rates & borrowing rates (deposits/FDs rates). Where the FY2023 period witnessed a robust expansion of NIMs across banks since lending rates increase first & borrowing rates/ deposit rates increase with a lag, several banks reported a record increase in their NIMs. Here is a chart to show how the NIMs have changed over period of 12 months in FY2023 (year ending March 2023):

Where most banks were able to increase their margins, banks like Kotak Mahindra, ICICI & Axis were able to increase them significantly. This happened because the overall cost of borrowing for these banks increased relatively at a much slower pace as RBI increased its rates. One of the key reasons was that these banks didn’t raise their deposit rates at a similar pace. But as the lag effect is kicking in, the overall cost of borrowing for banks still continues to increase with no increase in rates at which they give loans. Here’s a chart, again from JP Morgan, showing how the NIMs have contracted for several banks over the first 3 months of this fiscal year:

This compression in the margins/NIMs of the banks negatively affects the top line of all banks; the more the compression, the lesser the topline. As one may notice, when it comes to private banks, the ones which saw the highest margin expansion in FY2023, now suffer the most. Kotak Bank reported a higher NIM compression followed by Axis Bank and ICICI Bank; and HDFC Bank is able to protect its margins better.

Can opening more branches help you safeguard your NIMs?

About 6 months back, I wrote a blog on how banks that are focusing on branch expansion tend to lead on the front of deposits growth as well (blog link here). In 2022, HDFC bank alone opened about 1400 branches which was about 70% of the total ~2000 branches added by all major banks in the system in that year; simply HUGE! This helped them grow their deposits at 20% YoY in 2022. Similarly, IDFC First Bank grew their branches at 18% last year which helped them grow their deposits at 44% YoY. There are many factors at play, but branch expansion is one of the most important ones. The graph below shows how various banks focused on branch expansion last year:

After having a look at their branch expansion, here is how their deposit growth panned out for these banks in 2022 on a Y-o-Y basis-

HDFC Bank: 20%

IDFC First Bank: 44%

ICICI Bank: 10%

Kotak Mahindra: 13%

Bandhan Bank: 21%

Axis Bank: 10%

SBI: 9%

BoB: 15%

PNB: 7%

Considering the fact that the deposits grew ~11% in the system. Clearly, there seems to be a high correlation between your deposits growth & branch expansion. Since the benefit of the ‘Branch expansion strategy’ comes with a lag on the deposit growth front, the growth should continue to be on the higher side for banks like HDFC & IDFC First. In short, in this tech-driven world, branch expansion still helps with higher growth rate in the most basic act in banking which is gathering public deposits.

But does it help you with safeguarding your margins as well?

When your growth rates for deposits are already on the higher side, especially at a time when there is a scramble for deposits in the market, banks actually don’t need to offer higher rates on deposits to attract more customers. Recently, many banks including Axis Bank, SBI, and many more, had to come out with more lucrative rates on their FDs to attract customers to deposit their money in their banks where I personally too, parked my money for the time being. Here is an extension of a chart I used above where I show you how the same banks which focused on branch expansion in 2022, are getting benefitted significantly now. HDFC & IDFC First Bank lead the chart with very limited margin contraction as per the recently released quarterly results of all banks (for time period April to June 2023):

Where Kotak, Axis & SBI are witnessing the highest contraction due to a mixture of 2 primary reasons:

They were amongst the banks which benefitted the most when the NIMs were expanding in 2022 as deposit rates go up with a lag, as shown in one of the graphs above

A slowdown in their deposit growth rate, pushing banks to raise their rates & attract more customers, negatively impacting the margins.

Crux?

Understanding NIMs cycle when investing in banking & NBFCs is essential, especially when it comprises 35%+ weight of our primary index - Nifty 50. Through this blog, I try to draw your attention to the fact that opening branches has 2 major benefits which are linked to each other. It helps you to grow the customer deposits & have better control over your NIMs, especially when we are around the peak of the rate hike cycle. I know I haven’t covered various factors/aspects involved that are essential as well but I believe the banks which adopted the branch opening strategy stand to win & deal with the current storm better relatively.

I hope you enjoyed reading, support me by sharing with your friends and help me reach more potential readers!

See you in the next blog!

Disclaimers-

Personal & client investment/interest in the shares exist for banks mentioned above; this isn’t investment advice; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome.

You had mentioned that compression in NIM affects top line but since the compression is due to a rise in deposit rates, wouldn't that help banks in lending more as they now have more deposit funds and consequently lead to a rise in top line. It will affect the bottom line though and not the top line as per my understanding. Please clarify.