Revolutionizing how Indians buy insurance

PB fintech: Our top pick within the new-age companies

(Published on February 27, 2023)

Basics

History: PB Fintech’s primary subsidiary, PolicyBazaar was founded in June 2008 by Yashish Dahiya, Alok Bansal, and Avaneesh Nirjar. They started as a digital platform - website and app - where users can compare insurance policies & buy the best policy for themselves & their families. In June 2021, Policybazaar obtained the insurance broking license from IRADA and now has its own agents which sell policies, making them an omnichannel player from a pure digital player earlier.

The 2nd major subsidiary, Paisabazaar, was started in 2014 and is an online marketplace for all lending and investment products.

Size of subsidiaries: Just to give an idea about the scale of their business, since its inception, Policybazaar has witnessed 1.35 Crore unique transacting customers (~20 lakhs of which were added just in 2022) on its platform and Paisabazaar has ~35 lakh unique transacting customers till date(~10 lakhs of which came in 2022)

Founder: Mr. Yashish Dahiya, the founder of PB Fintech owns 4.6% of the company (can be higher because of ESOPs), and comes from an Army family. He was the first person in his family to not join Army, Navy, or Airforce but rather went on with his entrepreneurship journey to start the flagship platform Policybazaar

Investment Thesis

Focus on profitability: The company has been steadily focusing on profitability. On dividing its business into 3 components:

Policybazaar: EBITDA(adj) positive since last 4 quaters

Paisabazaar: Turned EBITDA(adj) positive in December 2022

Other/New initiatives: Losses falling from Rs 90 Cr (peak) to Rs 54 in Dec, 2022

The contribution margin of existing business has gone up from 40% to 44% YoY and shall increase further because of recurring/renewal business, which has a higher contribution (%) margin, becoming an increasing proportion of revenues, as guided by management.

Accelerated growth in revenues:

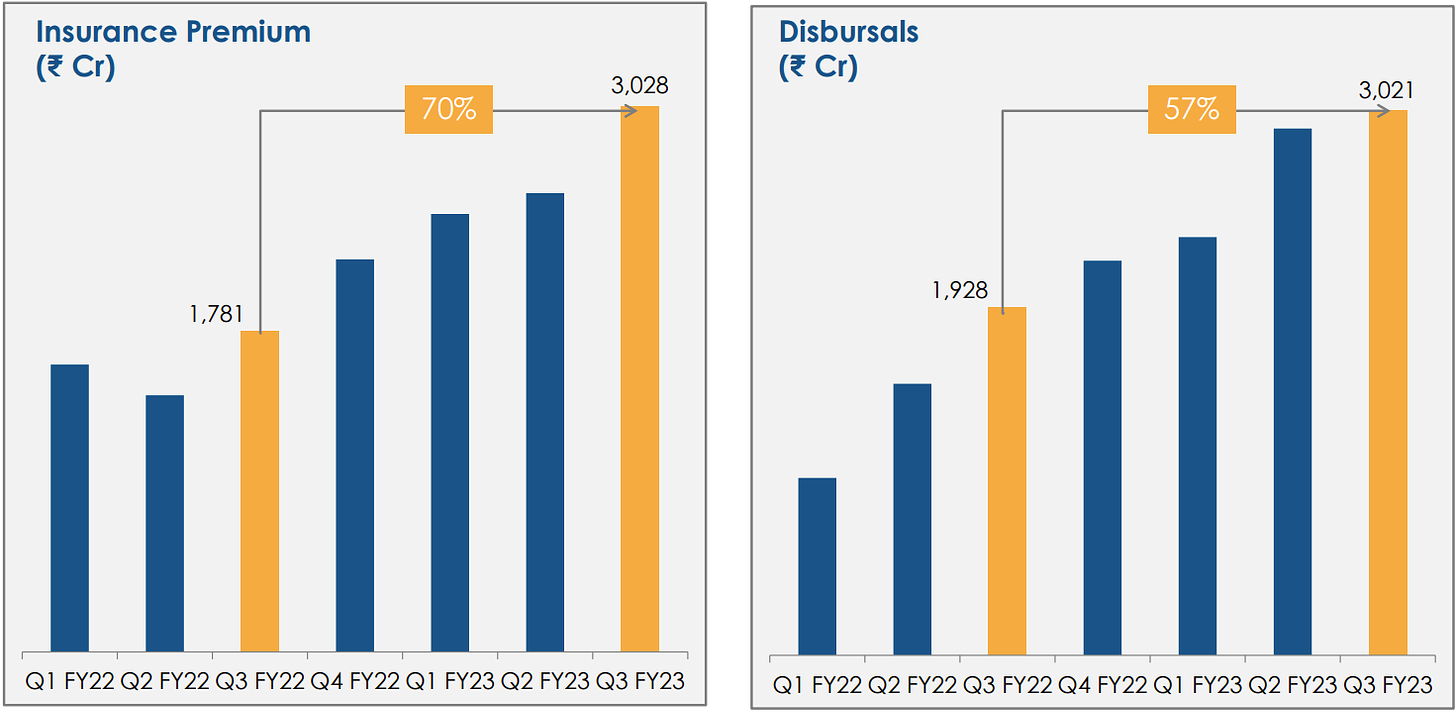

On the side of insurance premiums happening their platform, the growth is at 70% YoY as of Dec 2022. This is way higher than the industry growth which is growing anywhere between ~10 to ~20% across various segments.

The insurance penetration in India was just at 4.2% in FY21 and this signifies how long and lucrative this journey can be as the penetration in India grows to global levels

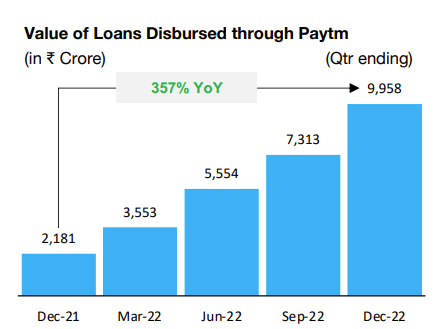

On the Paisabazaar side as well, the disbursals of credit grew by 57% YoY in the December quarter. Interesting to note that when compared to Paytm’s disbursal of loans, Paisabazaar stands nowhere. Paytm’s disbursals grew 357% YoY to reach about ~Rs 10,000 crores in a quarter against Paisabazaar’s Rs 3,021 crores worth of disbursal

Funding crunch for competitors: As the funding crunch globally continues for the startup ecosystem due to increasing interest rates & fed tightening, Indian startups in the online insurance market place like Digit insurance, Acko, and Phonepay (insurance) seem to have curtailed their aggressive customer acquisition strategy. After all, I don’t find Virat Kohli’s ads promoting Digit Insurance as often as I used to early in 2021 :)

This implies that Policybazaar has an opportunity to grow/maintain its market share via its strong brand name with limited spending on marketing or on customer acquisition.

Major Risks

New competitors entering the market: As we mentioned above, Paytm started its credit disbursal service only 2-3 years ago, against 8 years for Paisabazaar, but today, it’s disbursing 3X the amount of credit than Paisabazaar (see picture below). Paytm could leverage its huge network of existing users & cross-sold credit products to them, earning handsome revenues today. Such disruption can always happen. As the founder, Mr. Yashish Dahiya rightly accepts, “For companies like ours, in 10 years from now either the company will be very strong or the company will not exist.”

Continued global tightening & impact on global tech valuations: Tech valuations are greatly impacted by levels of interest rates in the economy & multiples at which global tech companies trade. With inflation coming down slower than expected, the Fed & global central banks would be forced to raise rates higher to curtail inflation, which might push global economies into recession.

Legal aspect & regulation: Both insurance & digital lending are highly regulated spaces. Any change in future rules & regulations by RBI or IRDAI or any relevant authority can have a significant impact on the way the business is conducted. This risk won’t go away, but can only be reduced via efficient compliance.

Decreased focus of government on savings/investments: It’s worth mentioning that insurance is a tax-saving product. The government in its recently announced budget has indirectly promoted the new-direct tax regime over the old regime by increasing the tax-free limit from Rs 5 lakhs to Rs 7 lakhs. This can influence more people to join the new regime wherein you don’t get any tax benefits on buying insurance policies. This trend of promoting the new regime might continue in the future as well.

Risk of existing PE fund exiting: There are still many early investors who would still be looking to exit their stake from the company, especially post the recent rally. This continues to be a major hangover for the stock.

I hope that helped you understand and make a better investment decision.

Liked it? why not share with friends & help this blog grow!

See you in the next post!

DYOR.

Disclaimers-

Personal & client investment/interest in the shares exist(as high as 10% of portfolio); this isn’t investment advice; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome

ESG standards influence the investment strategies