Can IDFC First Bank outperform all other Banks?

My most bullish banking stock in Bank Nifty

Wishing you a very happy, prosperous & healthy new year 2023!

*************

With credit growth shooting high, & deposit growth yet to catch up, banks have been forced to raise rates to encourage customers to deposit more money.

Deposits are used by banks to lend it further to borrowers & the differential in the interest rate of taking deposits from people & lending it at a higher rate is what they earn as banks in form of their income. Let’s take Axis Bank as an example before we move on to IDFC First Bank.

In the latest quarterly results, which is Q2 of FY23, Axis bank’s domestic loan book growth came in ~20% YoY & 4% QoQ. Whereas, their deposit growth came in at a 24-quarter low of just 10%.

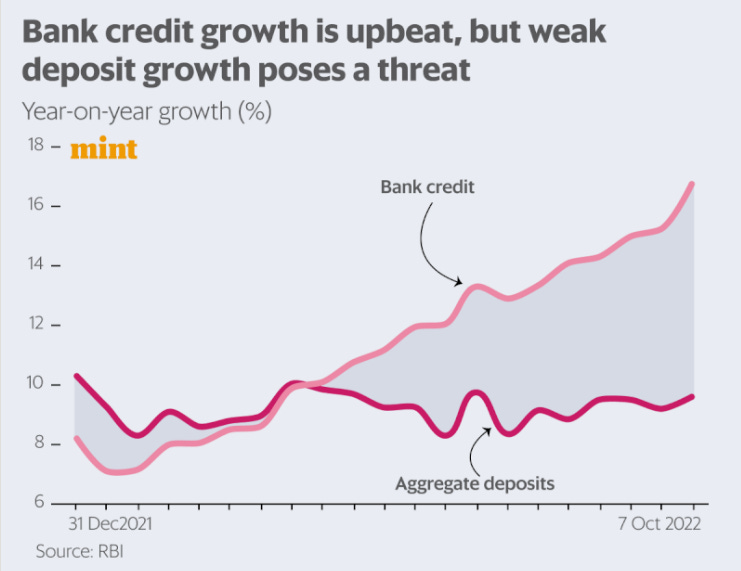

To give you more context, have a look at the following graph from Mint which explains how the credit growth (borrowings) has increased in the economy but the deposit growth hasn’t increased at that pace-

Where the deposit growth has been ~10% overall, the loan growth currently is as high as 18%! This differential of 8% is workable in the short run as generally, banks do have the previous sets of deposits that were unutilized or just parked with RBI in the past when loan growth wasn’t there, but not at all sustainable in the medium to long term.

This is the reason why the CEO of Axis Bank, Mr. Amitabh Chaudhry said recently, “It is not possible to sustain the current rate of loan growth with a lag in deposit growth”, in an interview with CNBC-TV18. Even the CEO of SBI, Mr Dinesh Kumar Khara came out and said that there is a ‘scramble for deposits’ currently.

Now that you got an understanding of what the banking industry today is dealing with, let’s move on to IDFC First Bank

ROCKET DEPOSIT GROWTH 🚀

Have a look at this chart which shows how the deposits with the bank in form of saving, fixed & current account deposits, etc. have grown over the last few years:

32% CAGR growth in the last 3 years which is getting accelerated in recent H1 FY23 is nothing else but mind-blowing.

Now comes the interesting part. While all this is happening, the interest rate that the bank is offering to its depositors has actually not moved much when compared to other banks. Have a look at this table I am trying you to focus on:

It’s very surprising how a bank can actually grow its deposit book so fast without any major increase in the interest rates it gives to its depositors on their deposits, which will directly impact its NIMs (Net interest margins), how was it possible?

Let’s try to find out!

The answer lies in franchise & brand building. IDFC First has positioned itself as a customer-centric bank that takes all its decisions keeping in mind the benefit & welfare of its customers. So similar lines are their ‘Near-Dear Test’ wherein every product that the bank offers goes through which the bank analyzes whether they are happy to offer the same product/service to its near and dear ones. Just recently, the bank also waived off fees on 25 commonly used banking services in saving accounts like the fee on the number of cash transactions, IMPS transaction cost, passbook charges, etc. These initiatives go a long way in brand building for the bank in eyes of its depositors.

The appointment of Amitabh Bachchan & the branding campaign the bank has been running on building trust has worked well for the bank.

BRANCH EXPANSION

IDFC First bank has increased its branches from 206 in December 2018(at the time of the merger) to 523 branches in September 2020 to 670+ branches today. Analysts might complain about the bank being heavy on operating expenses & rentals side, which actually is a drag on the profits, but has actually helped the bank in building the required trust & reputation in eyes of the public in general.

And if you thought that bank didn’t focus on digital side, then you are wrong again. IDFC First was amongst the few banks that RBI selected for experimenting its e-Rupee. Also, I personally believe that the user interface of IDFC First’s website & app is much better than the likes of HDFC bank who invests the most in technology of all banks.

This trust-building process with the intent of attracting customers, started by offering them higher interest rates, is today making the bank fire on all cylinders.

A small anecdote, if you remember the May of 2020 when the share prices of many banking stocks bottomed, the debate was still on about who is following the similar fate of Yes bank which collapsed in March 2020. The chances of IDFC First were not that low as well. But despite being a small bank, IDFC First Bank made a strategy of attracting more deposits at that time when the system had enough liquidity being pumped into by RBI(some Rs 9 lakh crores excesses I believe?). Well, the bank has covered a lot of ground on that front but has a huge distance to travel.

Share with someone who might be interested!

Risks & Note:

Investment in IDFC First bank is a high-risk investment, with the potential for exceptional return, following the probability of high loss.

The story of IDFC revolves around one man, the CEO V. Vaidyanathan, and not the team as of yet, which is again a risk.

They do spend a lot on marketing & brand building, getting many eyeballs & hence majorly owned by retail investors & not institutions yet.

The bank share is would fall the maximum incase an economic downturn or covid comes again because of the customer segment they serve.

DYOR.

Disclaimers-

Personal & client investment/interest in the shares exist(as high as 10% of portfolio); this isn’t investment advice; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome

Hey!

You summarize things really very well. I seriously want to learn how do you do such level of research.

How can we connect?

Thankyou!