Why investing in DLF made sense to us?

Analysing the Macros & Micros for you!

When you hear of Gurugram, the first thing that comes to mind is DLF. That reminds us about the potential real estate companies like these have in building a whole city from scratch. This blog isn’t a piece of investment advice, rather here we write about why we ended up investing in DLF.

Before we move on to the micros of DLF, let’s discuss the Macros & industry.

HOW IS MACROECONOMICS SET?

For real estate companies, the rate of interest is a big headwind in 2 ways. Firstly, interest rates rising encourage customers, not to buy property on loan, but wait for better times. Secondly, real estate companies tend to have a good amount of debt on their balance sheet for construction purposes, which can actually put them into trouble & even bankruptcy.

So last week, RBI again raised interest rates by 0.35%(negative for real estate), putting the Repo rate at 6.25%, & is expected to rise some more in the coming months. It does sound weird as you see the interest rates still rising & me giving a recommendation of buying DLF to you, right? Well, even though rates are rising, they aren’t expected to rise at a similar pace in the coming months as inflation (both CPI & WPI) cooled off last week & we believe, markets have already discounted the related negative impact of rate hikes that have happened as it usually takes some time to impact the real economy. As per recent research, until the borrowing rate of an average Indian borrower for a home loan doesn’t cross the 10-11% range(which it hasn’t yet), it won’t have a material impact on the borrower’s mindset to take a loan for his home.

On the construction side, let’s talk about cement(one of the main components in making buildings). Indian Cement industry has recently seen more of investments, Capex & interests from new (read Adani) & existing players, hinting towards more competition & more supply in the future, keeping prices in control (possible outcome). Even on the side of the metal, prices of various commodities have fallen significantly due to tightening from Fed & other global central banks this year.

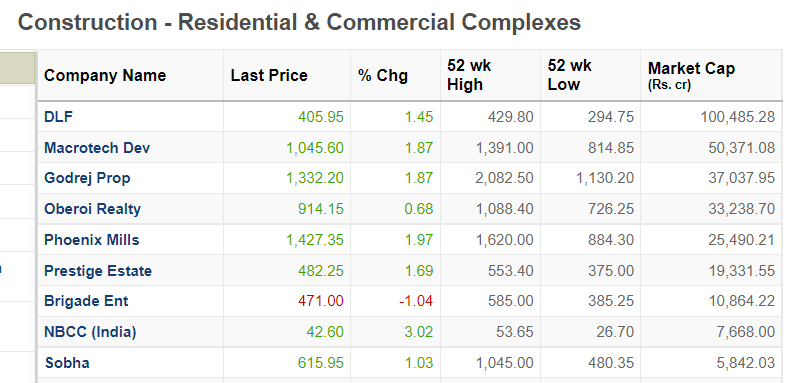

Let’s have a look over related firms & see how big they are compared to DLF, before talking about the company. Here is a list of the top 9 companies involved in Residential & commercial complexes in terms of market cap: DLF is the biggest in the size & double the size of its nearest competitor in terms of market cap.

Let’s discuss DLF now:

So DLF majorly has 2 components from where it derives its revenues- Residential & Rental business. In my personal view, the Rental business is the key value driver for DLF despite the residential business being the key revenue driver. This is because when DLF started to expand & build its brand in Gurugram, it was DLF Cybercity- the office rental, which helped the company build the value, trust & luxury feel in minds of Indians about what DLF can do. This legacy has continued to be built on numerous projects completed & delivered.

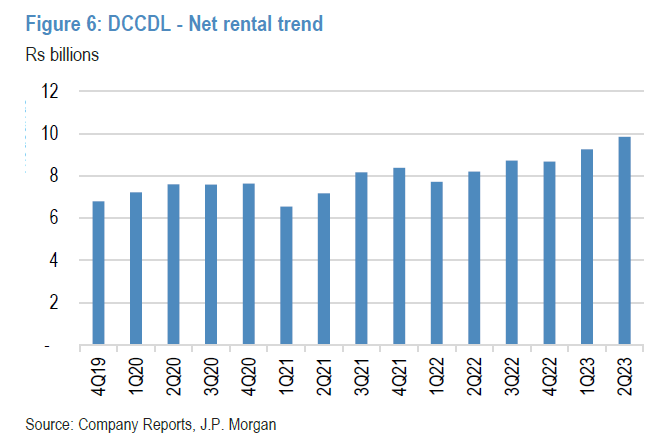

DLF RENTAL (DLF Cyber City Developers Limited (DCCDL) - 67% owned by DLF)

This chart is of the revenues earned by the flagship company of DLF, DLF Cyber City Developers Ltd., which is involved in the development of commercial properties.

Do you see that dip in 1Q21? That’s the first lockdown yes! Since then, the company has made superb progress with net rental inflows almost touching ~Rs 1,000 Cr ( ~Rs 10 billion) from below Rs 800 Cr in pre-pandemic.

Looking from a macro perspective here, the Commercial rental business in India is set to grow well in the coming years as more & more companies throughout the world come forward to increase their capabilities from offices based out of India. A recent example of National Australia Bank occupying 50,000 sq ft in a WeWork, which is based just in front of DLF Cyberhub. Do consider consulting companies like Mckinsey even plan to double down their workforce here in India in the coming years & shall generate high demand for premium rental spaces, where DLF is a king in itself.

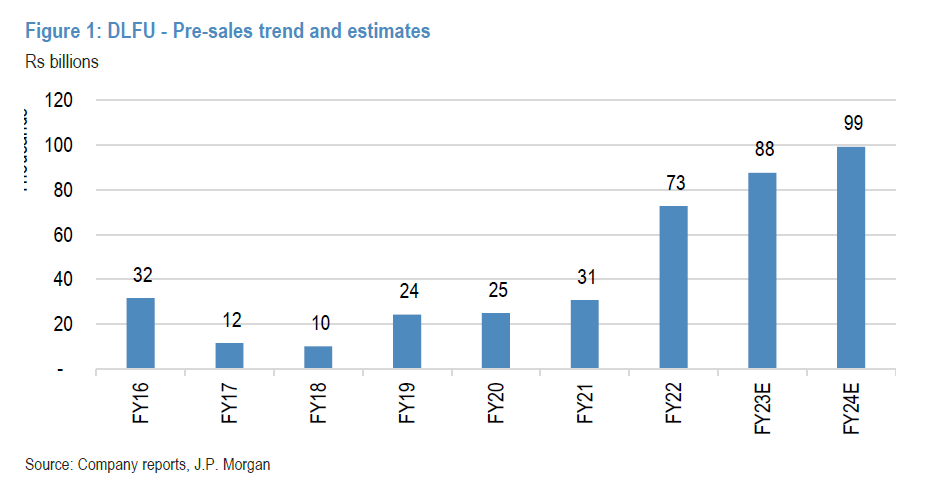

DLF Residential Business (DLFU)

The premium flats & houses DLF construct, are actually sold generally in a scheme where in some proportion (say 25%) is the downpayment the buyer of the flat has to pay even before the construction for the property has started & the rest is paid in a deferred manner/at the time of possession. As per accounting practices, amount received on properties sold via this Pre-sales, become deferred revenue for DLF & here’s a trend of this:

This chart helps us understand the potential growth in pre-sales that DLF can deliver seeing the current projects in its pipeline. There is a huge pipeline of properties DLF can have for sale within Gurugram itself as more & more people looking to rent or buy properties there as more & more companies ask their employees to work from the office.

Let’s see some risks now.

Not the cleanest bookkeeper: The accounting embezzlement practices in properties are quite easy & DLF also has been stuck in cases related to land acquisition (remember Robert Vadra’s link with DLF making headlines in 2012-13?) & many other cases. The ask from them would be for more detailed disclosures to improve transparency & best in class governance.

Macro interest rate headwind: If the interest rates continue to rise strongly, it can soon become a major deterrent for home buyers to delay their purchase decision & DLF, being amongst the largest real estate player in India, can get a stong hit.

Share with someone who might be interested!

Disclaimers-

Personal interest in the shares exist; this isn’t investment advice; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome