Why we recently invested in Coal India?

Dividend play getting stronger with upcoming central elections of 2024

Recent Happening

Not particularly regarding Coal India, but one news that left Gujrat-based PSUs like GSFC & GSPL skyrocketing last week, was this ⬇️ where the government of Gujrat changed the dividend payout policy for its PSUs, aligning them as per Central government norms of 2016 for CPSEs, where they now need to payout at least 30% of profits earned as a dividend.

About Coal India

Coal India is among the world’s largest producers of coal, producing more than 700 MT of coal in a year, which is ~80%+ of India’s total production of coal, supplying it to numerous thermal power plants across states. Interestingly, even 700 MT is not sufficient to meet India’s energy demands via coal, hence India is an importer of coal today, importing 150+ MT of Coal in FY23

Regarding financials and the stock, Coal India has generally been considered as a ‘Value’ investment with very low growth aspects in the future. It’s a big cash machine, producing over Rs 30,000 Crores in operating cashflows and a similar amount of net profit. With a market cap of ~Rs 140,000 Crores, here are a few ratios that you might find interesting:

Price-to-earning (PE FY23 E): ~ 5 times

Dividend yield: 10%+

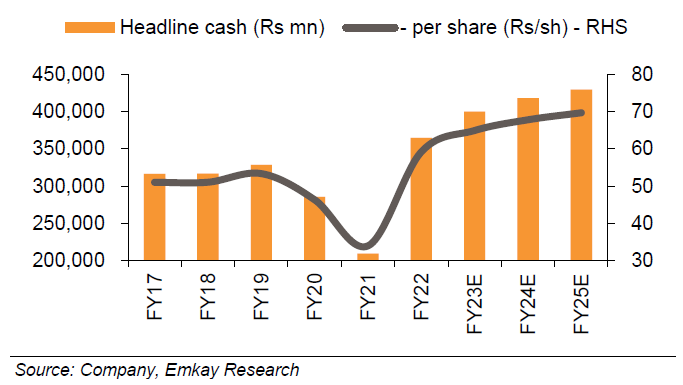

Cash per share on books: ~Rs 70 per share, against a share price of ~Rs 230, which makes about 30% of its share value coming just for cash! Here’s a chart to show how much cash Coal India has on its books⬇️:

Investment Rational

We recently invested in Coal India for the first time, giving it a small weightage in our client portfolios, and here’s why:

Upcoming National Elections of 2024: We expect strong/higher dividend payouts in coming quarters and the reasoning for the same is mentioned below ⬇️

The preparations for the central elections of next year are already on and the BJP government would look to get their 3rd term. One of the key misses of the current government has been on the front of the disinvestment front where the government has consistently failed to meet its budgeted disinvestment targets year after year by huge margins. Even though the government tasted some successes like the sale of Air India, a major part of it was also because of the buyer’s reputation as Tatas are known for never asking their employee to leave. So there was a sense of security in the eyes of employees of Air India and good public perceptions of Tatas obviously helps in convincing the general public that the deal is a great deal!

Even though the tax buoyancy in the economy has made up for the targets missed on the disinvestments front, there’s a strong possibility that government looks to boost its income and hence spending ahead of the elections 2024. Where disinvestments come with the disadvantage of the image of BJP getting tagged as an anti-labor/anti-government employee party, possibilities of strong actions on the disinvestments front seem to be low. Rather we think that the government will be expecting higher dividends from its PSUs to fill the gap caused due to not meeting disinvestment targets. And since PSUs are owned by the government itself, we expect the government to push PSUs to improve efficiencies further and payout a higher dividend from their income.

Moreover, a recent report by a top investment bank covering ITC (India’s largest cigarette manufacturer) came out with a note that ESG factors are not deterring the FIIs to own more of its shares. Similarly, in the case of Coal India, where ESG plays a key role since burning coal isn’t appropriate for the environment (E of ESG), if the dividend yield goes up, it won’t deter the FIIs from owning it. No wonder why someone like JP Morgan has had an overweight call on Coal India for 3 years+ now.

Key Risk

As of Feb’23, everyone was very bullish about India’s power consumption touching new highs in the coming summer season after a hotter-than-average February. Even the probability of El Nino was predicted to hit India in about 2-month which would lead to hotter-than-average summers.

Fast forward to now, both March and April turned out to be much colder than averages in past years, negatively affecting the demand for power. Hence the prices of electricity on IEX are currently lower compared to the last 2 years. Low electricity demand, means low demand for coal at thermal stations, and that directly affects Coal India.

Political/government-related risks are again key risks that exist when you invest in PSUs. As you saw the Government of Gujrat changed its policy in favor of shareholders (read ‘for ownself’) this time. This can reverse as well in the future which is a big risk for shareholders of PSUs. They are controlled by the government after all and the government’s motives are often different from those of shareholders.

FY 2023 and beyond…

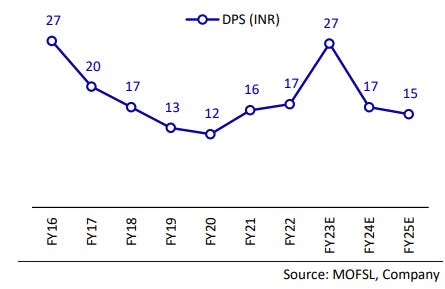

For FY23, COAL has already declared 2 interim dividends totaling INR 20.25 per share, and few brokerages expect a further dividend of ~INR 7 as the final dividend for the year (Update: actual dividend came in at INR 4, making the total as INR 24 for FY23). Motilal Oswal estimates the dividend per share to fall in FY24 and FY25 as shown below to INR 17 and INR 15 and that’s where I think Coal India can surprise on the upside, especially for FY24 which would also be marked as the key year before elections.

Thank you for reading, that’s all for this blog.

DYOR before investing.

Disclaimers-

Personal & client investment/interest in the shares exist; this isn’t investment advice; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome