Will The Elephant Dance Soon?

How HDFC Bank's comeback is being hindered by SBI's resurgence

India’s largest private banks (HDFC and Kotak Mahindra Bank) reported a mixed bag in their Q1 results recently. In the results conference call, HDFC’s CEO, Sashidhar Jagdishan, acknowledged that deposit growth was somewhat disappointing but expressed confidence that the full-year results might surprise analysts. While most performance metrics met expectations, NPAs increased quarter-on-quarter. Whereas, Kotak Mahindra Bank faced a sharp contraction in margins.

Even though banks like HDFC are making strong efforts to regain their former glory, we believe it still has a long way to go. While the systemic issues continue which we highlighted in the January 2024 blog when we outlined our bearish view of HDFC Bank, in today’s blog we write on why we continue to have a bearish outlook for the bank over the medium term (1-2 years). We plan to write another update by the end of the year to keep our readers informed about how our perspective is evolving. We would recommend reading our previous 2 blogs on HDFC Bank of 2024 for better context, before reading today’s one:

Did the elephant fall while dancing? (January 2024)

Is the Elephant back in the ring? (April 2024)

We hope you enjoy reading this blog, let’s get started!

Is the Golden Phase for Private Banks Over?

Indian banking experienced several major shocks between 2010 and 2020. This period saw the emergence of significant NPAs (Non-Performing Assets) for banks involving prominent names such as Kingfisher Airlines, Bhushan Steel, ABG Shipyard, Amtek Auto, Essar Steel, Jaypee Infratech, Gitanjali Gems, and Electrosteel, among others.

In 2014, the political landscape in India changed, bringing the harsh realities of the banking sector to light. Public sector banks (PSU banks) suddenly faced the burden of thousands of crores in bad loans, particularly in the infrastructure, steel, and power sectors, due to poor lending practices and inadequate risk assessment.

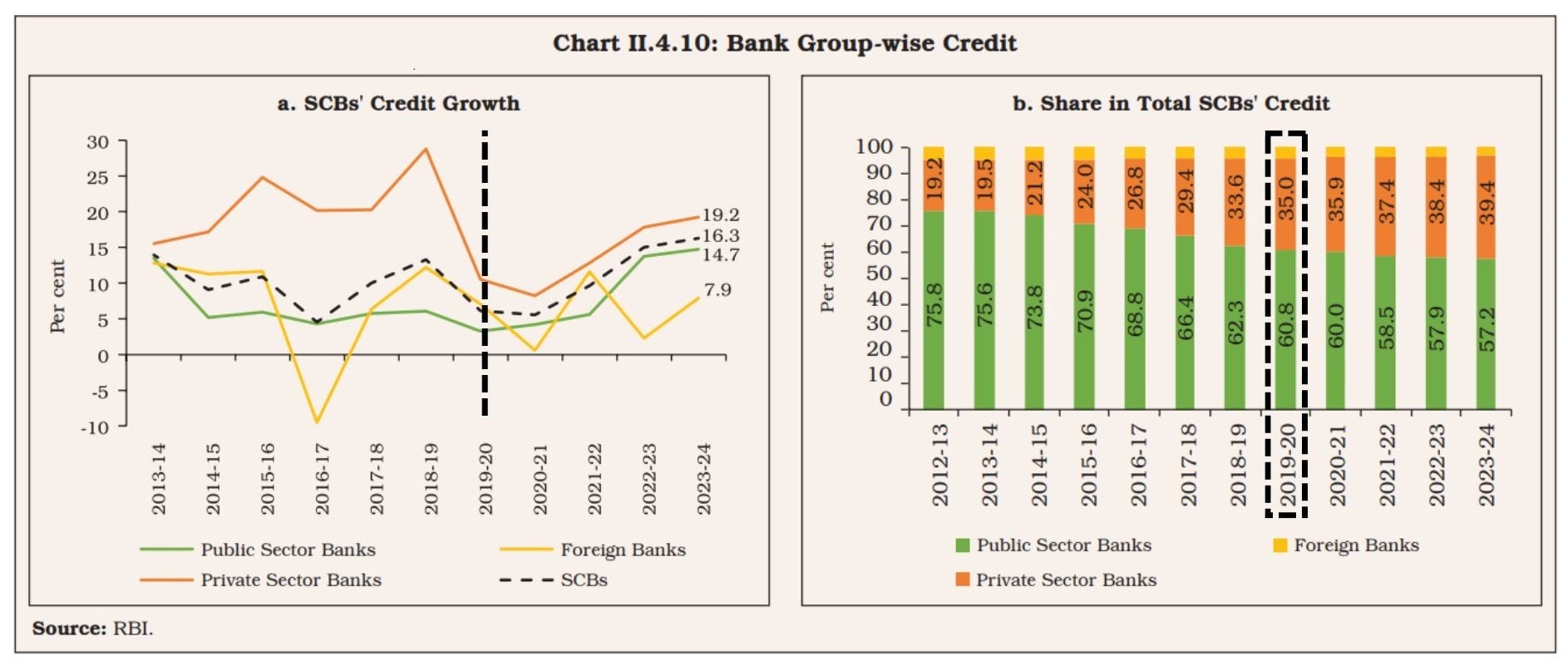

These NPAs choked the PSU banks to such an extent that the former finance minister - Arun Jaitley, had to announce the recapitalisation of Public Sector Banks (PSBs) to the tune of Rs. 2.11 lakh crore in October 2017. Due to poor performance, these banks already suffered from low valuations and were not in a position to raise capital from the market through QIPs, which necessitated Arun Jaitley's intervention. The biggest beneficiaries of this situation were their private counterparts, who doubled their market share of lending over the last decade as shown in the graph.

(SCBs, or Scheduled Commercial Banks, refer to the overall banking system.)

As shown in the left chart, public sector banks continued to experience slow growth due to ongoing troubles, fresh NPAs, and a low equity base. In contrast, private sector banks saw their books grow by 20% to 30% during the pre-COVID period, while public banks grew at an average rate of just 5%, which was sometimes below the prevailing inflation rate.

However, since COVID hit, the gap in growth rates between public and private banks has significantly narrowed. PSU banks have started to grow at a decent pace, approaching, if not matching, the speed of private banks. As a result, the rate at which public banks lost market share to private banks has significantly reduced post-COVID.

Amongst, the biggest beneficiary of PSU banks losing market share was HDFC Bank which was able to double its share in less than 10 years by FY23:

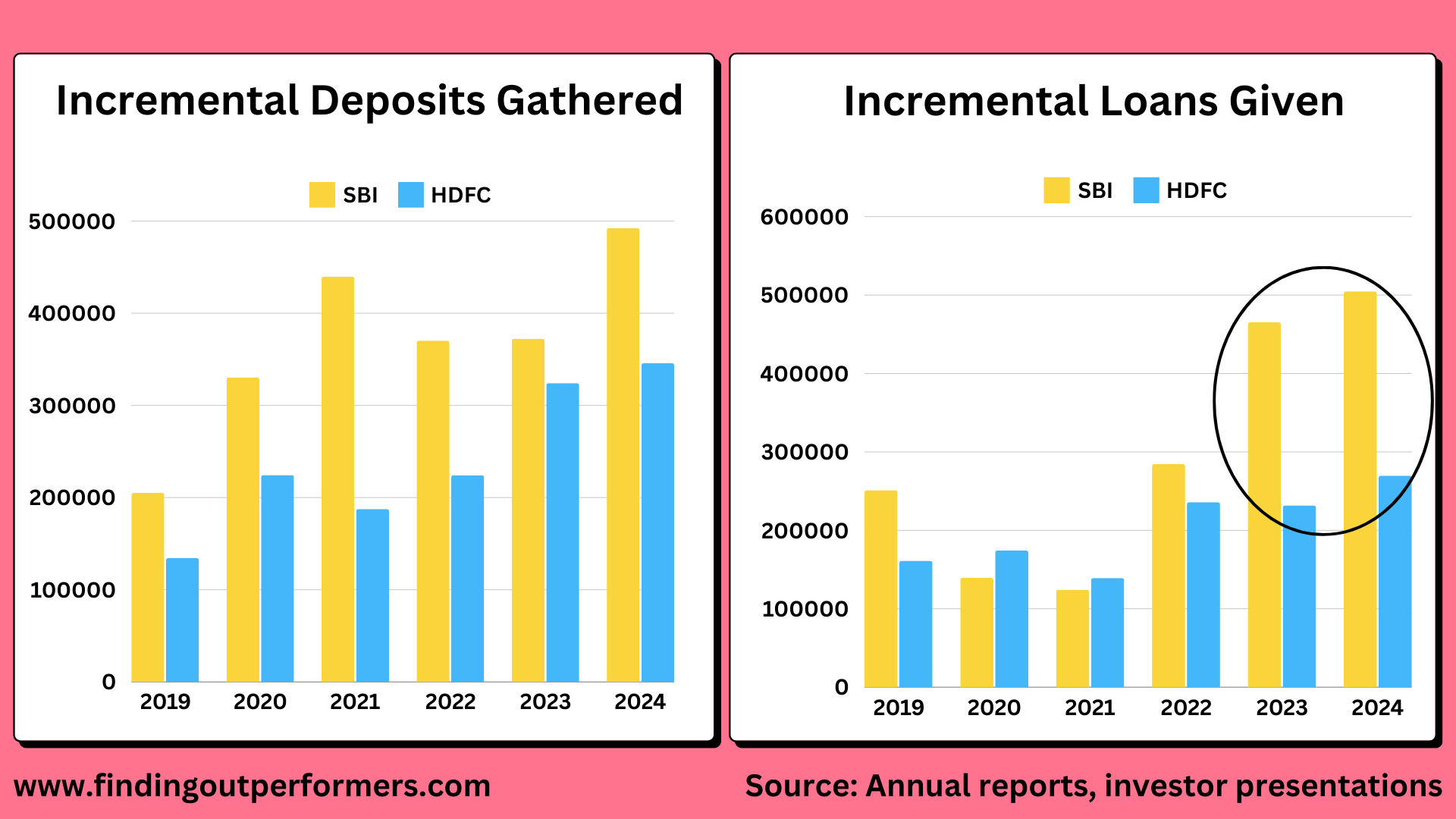

However, this pace of gaining market share has been significantly impacted for HDFC over the last 2 years on the front of the advances (after adjusting for the merger). Here is a chart depicting how HDFC has been able to grow its incremental deposits at a good pace, but SBI has been able to widen the gap between the two when it comes to incremental loans given by both (in Crore Rs) as HDFC bank continues to struggle due to its merger. Do note, SBI continues to be the biggest bank in India, with over 20% market share.

PSU banks are no longer dependent on the government for recapitalization, as they were in 2017. Due to ongoing market buoyancy and share prices rising up to 5X in the last five years, these banks can now easily raise capital independently whenever necessary. Just some time ago, an Economic Times article reported PSU banks like PNB, Bank of Maharashtra, Union Bank of India and more banks planning to raise up to Rs 40,000 Crores in the coming 6 months via QIP.

Opening branches - A desire or a necessity?

One of the key reasons HDFC has successfully grown its deposits and gained market share is its aggressive branch expansion strategy, particularly in the years following COVID. The bank has been opening new branches across Tier 1, 2, and 3 cities since the last few years as shown in the graphs below.

At the time of the merger between HDFC Bank and HDFC Ltd, the management had set an ambitious target to continue this expansion, aiming for 1,400-1,500 new branches in FY24. Their medium-term goal was to increase the total number of branches to 13,000-14,000. However, they later adjusted this target to a slightly lower number for the immediate future.

It's important to note that SBI has not been opening branches aggressively because it already has an extensive network of 22,000 domestic branches, compared to HDFC Bank's 8,700.

Aggressive branch expansion comes at a cost. It affects the overall cost-to-income ratio due to increased rental expenses, higher operational costs, and the need to expand the workforce. For example, HDFC Bank’s employee base grew from 88,000 in 2018 to over 173,000 in 2023, which further touched 213,000 in 2024 due to its merger with HDFC Ltd.

In contrast, SBI has focused on improving efficiency and has reduced its workforce from 264,000 in 2018 to 232,000 today, representing a decrease of 32,000 employees at a government bank.

HDFC Bank Vs SBI

While opening multiple branches isn’t an issue if it aligns with your medium- to long-term goals, we believe it has become a necessity for HDFC Bank at perhaps the most challenging time. We will explain why we think so through 3 points-

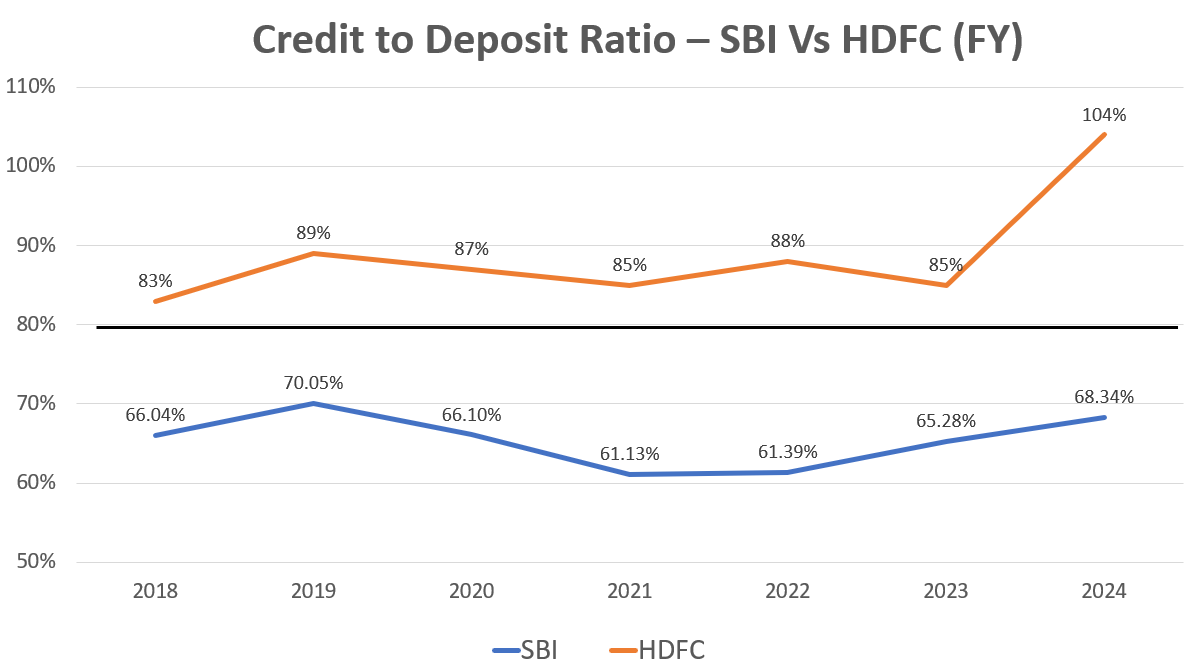

Credit to Deposit Ratio - This ratio measures how much a bank lends out of the deposits it raises. It has gained increased relevance over the past year, particularly due to repeated soft warnings from the RBI. The Governor has explicitly emphasized the need for a 'correlation' between credit growth and deposit growth for all banks, holding regular meetings to discuss this issue.

Over the previous decade, the Credit-Deposit (CD) ratio was comfortably within the range of 70-80% for the banking system. However, post-COVID, this ratio has increased for most banks, especially private ones, with some banks now having ratios exceeding 100%.

For every Rs 100 in customer deposits, SBI has issued loans amounting to Rs 68, whereas HDFC Bank has issued Rs 104 (a sharp rise due to the merger with HDFC Ltd). Considering the 80% benchmark that the RBI is reportedly aiming for, they will have to bring it down at a faster pace. Whereas SBI has considerable room to expand its loan book faster and aggressively gain market share, even if its credit growth lags its deposit growth for the next few quarters.

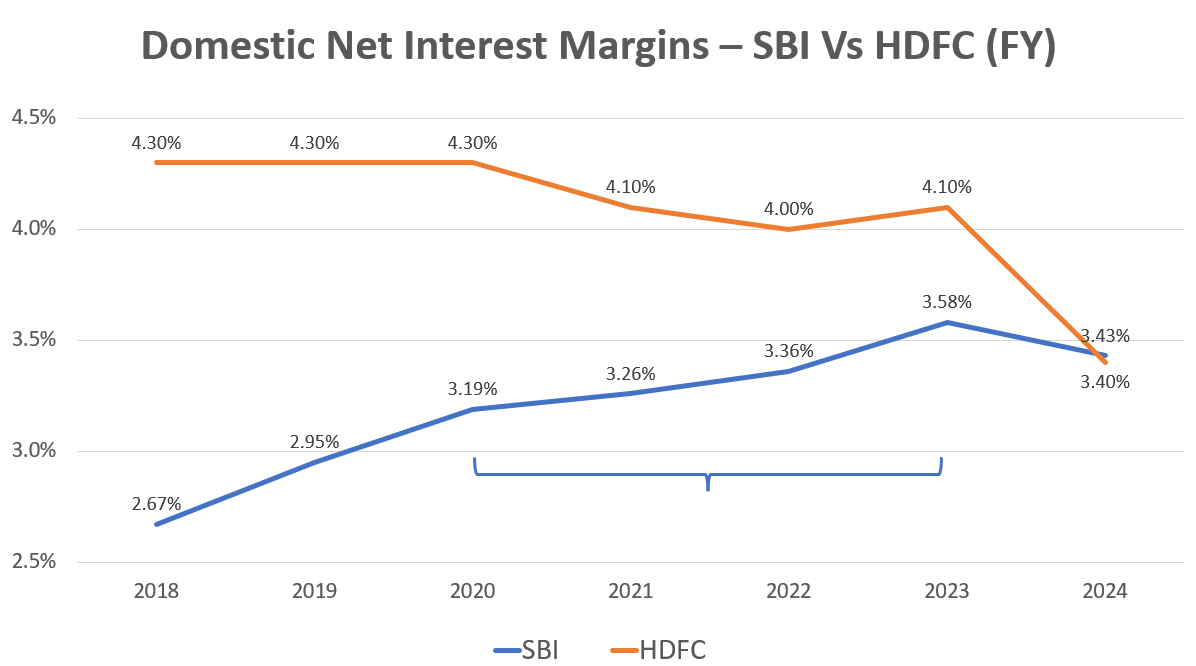

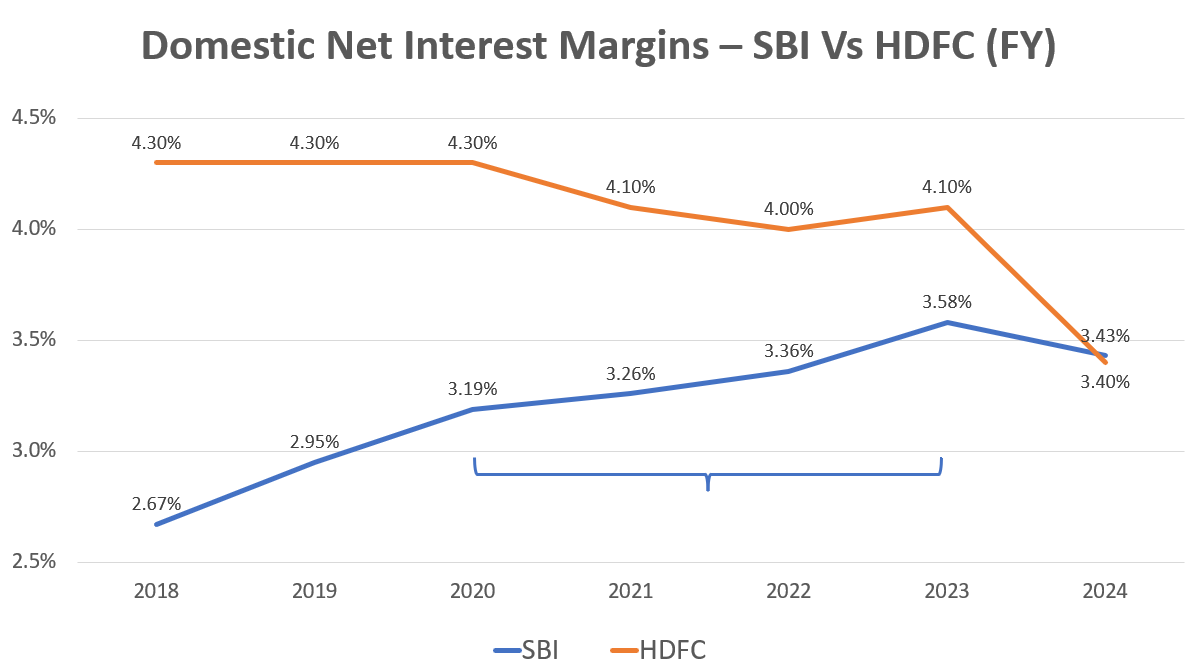

Net Interest Margins (NIMs)- The Net Interest Margin (NIM) represents the difference between the interest rate a bank charges on loans and the interest rate it offers on deposits (such as fixed deposits and savings accounts). Even before HDFC Ltd’s merger with the bank in July 2023, India’s largest private bank had been experiencing a clear downtrend in NIMs since the onset of COVID. In contrast, SBI had already been expanding its NIMs pre-COVID, due to an increased focus on retail loans which have higher margin. This trend continued from FY20 to FY23, while other private banks like HDFC Bank struggled.

As a result of the merger, HDFC Bank’s NIMs fell below SBI’s domestic NIMs by March FY24, a scenario that would have been unexpected about a year ago.

This impressive performance now gives a lot of headroom to SBI to offer attractive rates to customers to corner large sums of deposits even if it comes at a cost of little NIM compression in the near future. Just recently, SBI introduced "Amrit Vrishti," a term deposit scheme with 7.25% annual interest on 444-day deposits, effective from July 15, 2024. Senior citizens receive an additional 0.50%, available until March 31, 2025.

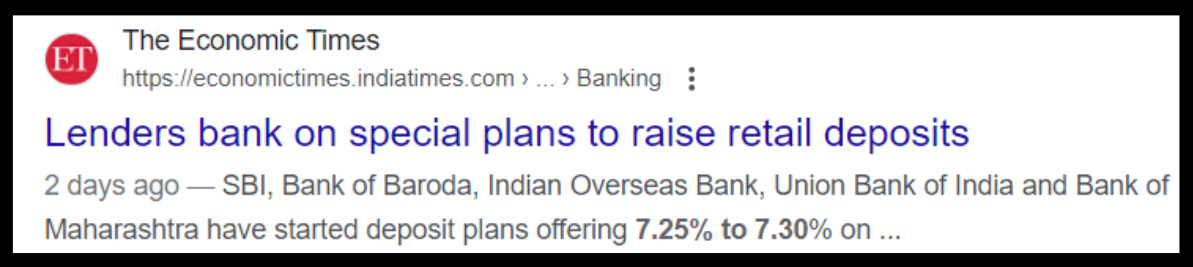

Competition from other banks: Recently in July 2024, RBI Governor Shaktikanta Das also held a meeting with the heads of public sector banks and select private sector lenders where he spoke about the high credit-deposit ratio of the system and the need to bridge the gap on deposit raising side.

The impact? It is not just SBI that immediately launched its 444-day deposit scheme, many PSU banks including Bank of Baroda, Indian Overseas Bank, Union Bank of India and Bank of Maharashtra have also now started deposit plans offering 7.25% to 7.30% on investments stretching from 399 to 444 days from July 2024, further fueling the fight for deposits.

Add to it the fierce competition HDFC Bank is facing from big private players like Axis, ICICI & Kotak Banks with all of them having CD-ratio above 80% right now, along with the systemic issues on the deposits front don’t appear to be resolving themself anytime soon.

To summarize the 3 points: HDFC Bank faces challenges due to its deteriorated CD ratio compared to SBI, slow momentum on NIMs relative to SBI's significantly higher NIMs before COVID-19, and the RBI's pressure on all banks to grow deposits faster. This situation leaves HDFC Bank with limited options to open more branches and attract additional deposits (at high operational costs), while also offering competitive rates on fixed deposits. Furthermore, the RBI Governor expressed concern on July 19, 2024, about household savings shifting to riskier assets like equities and mutual funds rather than staying with banks. For your reference, we've included a video link below.

“There could be structural changes happening which lenders need to recognize …. Household savings are increasing turn to capital markets & other intermediaries over bank deposits. They are allocating a greater portion of savings to mutual funds, insurance funds & pension funds.”

- Shri Shaktikanta Das, RBI Governor

Is HDFC Bank technologically well-placed?

In this era of digitization, almost everything has moved online—from shopping on Amazon and Flipkart to ordering food through Swiggy and Zomato. Consequently, another way to increase market share in deposits is by implementing advanced & customer-friendly tech that attracts more people to open accounts with your bank. While opening more branches across cities can indeed bring in more deposits, having robust technology in place can also significantly enhance customer acquisition and retention.

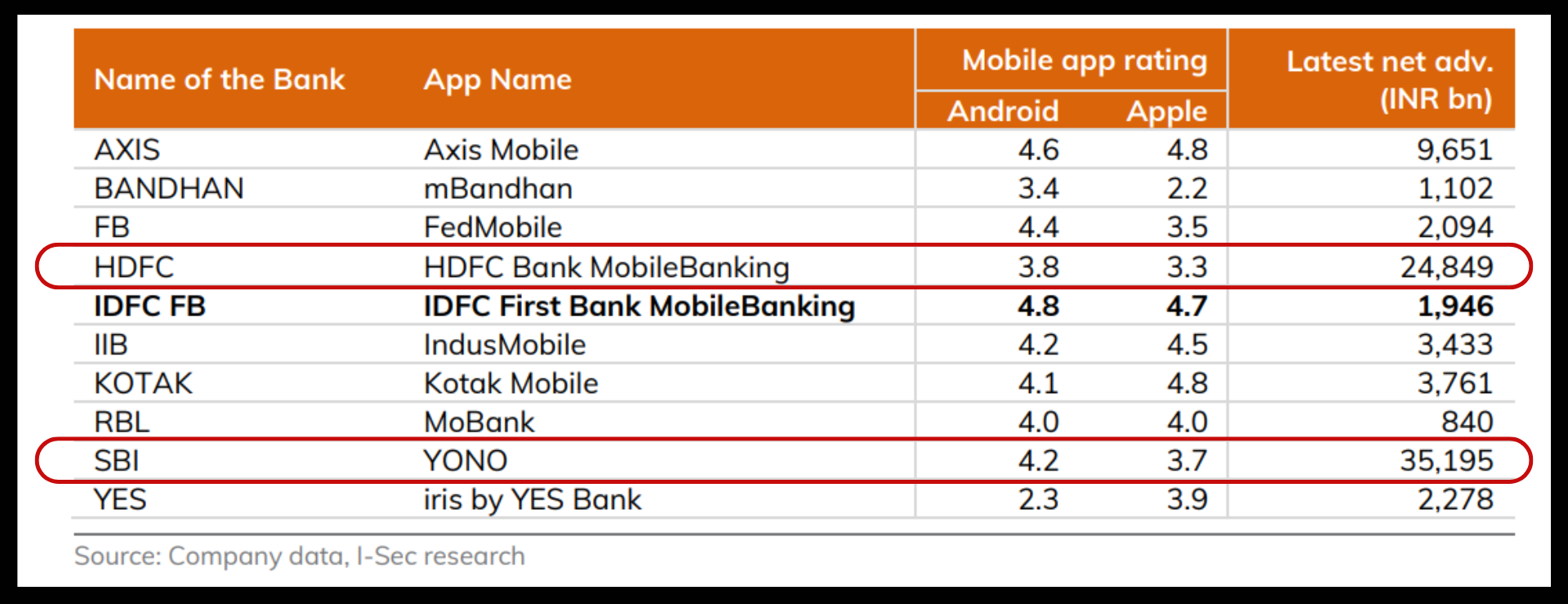

But despite having information technology (IT) spending being 7% of their total expenditure, HDFC lags significantly on various digital banking experiences highlighted in the average ratings they have for their banking apps. One must note that even RBI had to push HDFC bank on several occasions in past to improve its tech. In fact in Dec 2020, RBI had ordered HDFC Bank to temporarily stop all launches of its digital business-generating activities following incidents of service outage over the previous two years. Similar action was also taken by RBI on Kotak Mahindra Bank just recently.

SBI’s banking app, YONO, has a much better rating compared to HDFC Bank's app. Additionally, SBI is set to launch YONO 2.0 soon, which has the potential to be a game-changer in enhancing customer experience.

Will SBI’s YONO 2.0 make a big difference?

SBI launched its mobile banking app, YONO (You Only Need One), in November 2017, marking a significant step in the bank’s digital journey. Today, YONO and YONO Lite have around 10 crore registered users. The upcoming launch of YONO 2.0 is particularly noteworthy because of the involvement of Nitin Chugh, the former CEO of Ujjivan Small Finance Bank. For the past 27 months, Chugh has been working quietly on enhancing this digital platform, which is currently undergoing trials with selected customers before its full launch.

Nitin Chugh led the digital transformation at HDFC Bank from 2013 to 2019, playing a crucial role in establishing their credit card business, which now holds the highest market share of 20%. In 2019, he became the CEO of Ujjivan Small Finance Bank but resigned within two years due to a dispute with the founder. Following this, he was offered the role of heading the digital banking segment at India’s largest bank, SBI. He is now preparing to launch the results of his work, with the new YONO 2.0 expected by the end of the year. If this initiative goes well, it shall be a game changer for SBI and big achievement on digital front. Read more about YONO 2.0 here.

To Summarize

During Modi’s first term, banks that depended on government recapitalization are now able to raise significant funds via QIPs. Banks like SBI have improved their margin profiles due to a changing loan mix, with a greater emphasis on retail loans—an area HDFC Bank is also targeting to accelerate its NIM growth.

In a scenario where systemic issues with deposits continue to concern the central bank, SBI's resurgence, coupled with its renewed focus on technology through YONO 2.0, could make it challenging for private banks like HDFC Bank to reclaim their former glory in the medium term.

*******************************************

We hope you enjoyed reading the blog. You can find Aditya here and Yash here. Let us know your feedback or what more you want us to cover on HDFC Bank.

Read our previous publications:

Wondering how you can support us?

If you find our content valuable & are willing to support, show some love here⬇️

Disclaimers-

We are not a SEBI registered advisor; personal investment/interest in the shares exists for the company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the decision maker is responsible for any outcome.

| A guest post by

|

By the way, a lot of the small finance banks are getting to value territory. Would be interested if you were to write on it.

I would be very interested in knowing the quality of the retail loans of SBI vis-a-vis HDFC. Also, I find it rather interesting that FIIs have been selling HDFC and Kotak. For Axis, SBI their share has been constant or has gone up marginally.